# Table of Contents

- [

Documentation page not found

- Read the Docs Community ](#-documentation-page-not-found-read-the-docs-community-)

- [User Guide — PyPortfolioOpt 1.4.1 documentation](#user-guide-pyportfolioopt-1-4-1-documentation)

- [Expected Returns — PyPortfolioOpt 1.4.1 documentation](#expected-returns-pyportfolioopt-1-4-1-documentation)

- [User Guide — PyPortfolioOpt 1.5.4 documentation](#user-guide-pyportfolioopt-1-5-4-documentation)

- [Expected Returns — PyPortfolioOpt 1.5.4 documentation](#expected-returns-pyportfolioopt-1-5-4-documentation)

- [Risk Models — PyPortfolioOpt 1.4.1 documentation](#risk-models-pyportfolioopt-1-4-1-documentation)

- [Installation — PyPortfolioOpt 1.4.1 documentation](#installation-pyportfolioopt-1-4-1-documentation)

- [Risk Models — PyPortfolioOpt 1.5.4 documentation](#risk-models-pyportfolioopt-1-5-4-documentation)

- [Installation — PyPortfolioOpt 1.5.4 documentation](#installation-pyportfolioopt-1-5-4-documentation)

- [Mean-Variance Optimization — PyPortfolioOpt 1.5.4 documentation](#mean-variance-optimization-pyportfolioopt-1-5-4-documentation)

- [Mean-Variance Optimization — PyPortfolioOpt 1.4.1 documentation](#mean-variance-optimization-pyportfolioopt-1-4-1-documentation)

- [Other Optimizers — PyPortfolioOpt 1.4.1 documentation](#other-optimizers-pyportfolioopt-1-4-1-documentation)

- [Post-processing weights — PyPortfolioOpt 1.4.1 documentation](#post-processing-weights-pyportfolioopt-1-4-1-documentation)

- [Other Optimizers — PyPortfolioOpt 1.5.4 documentation](#other-optimizers-pyportfolioopt-1-5-4-documentation)

- [Post-processing weights — PyPortfolioOpt 1.5.4 documentation](#post-processing-weights-pyportfolioopt-1-5-4-documentation)

- [Plotting — PyPortfolioOpt 1.5.4 documentation](#plotting-pyportfolioopt-1-5-4-documentation)

- [Plotting — PyPortfolioOpt 1.4.1 documentation](#plotting-pyportfolioopt-1-4-1-documentation)

- [Roadmap and Changelog — PyPortfolioOpt 1.4.1 documentation](#roadmap-and-changelog-pyportfolioopt-1-4-1-documentation)

- [FAQs — PyPortfolioOpt 1.5.4 documentation](#faqs-pyportfolioopt-1-5-4-documentation)

- [FAQs — PyPortfolioOpt 1.4.1 documentation](#faqs-pyportfolioopt-1-4-1-documentation)

- [Contributing — PyPortfolioOpt 1.4.1 documentation](#contributing-pyportfolioopt-1-4-1-documentation)

- [Roadmap and Changelog — PyPortfolioOpt 1.5.4 documentation](#roadmap-and-changelog-pyportfolioopt-1-5-4-documentation)

- [Citing PyPortfolioOpt — PyPortfolioOpt 1.5.4 documentation](#citing-pyportfolioopt-pyportfolioopt-1-5-4-documentation)

- [Contributing — PyPortfolioOpt 1.5.4 documentation](#contributing-pyportfolioopt-1-5-4-documentation)

- [Python Module Index — PyPortfolioOpt 1.5.4 documentation](#python-module-index-pyportfolioopt-1-5-4-documentation)

- [Search — PyPortfolioOpt 1.4.1 documentation](#search-pyportfolioopt-1-4-1-documentation)

- [About — PyPortfolioOpt 1.5.4 documentation](#about-pyportfolioopt-1-5-4-documentation)

- [About — PyPortfolioOpt 1.4.1 documentation](#about-pyportfolioopt-1-4-1-documentation)

- [Python Module Index — PyPortfolioOpt 1.4.1 documentation](#python-module-index-pyportfolioopt-1-4-1-documentation)

- [Search — PyPortfolioOpt 1.5.4 documentation](#search-pyportfolioopt-1-5-4-documentation)

- [Black-Litterman Allocation — PyPortfolioOpt 1.5.4 documentation](#black-litterman-allocation-pyportfolioopt-1-5-4-documentation)

- [Black-Litterman Allocation — PyPortfolioOpt 1.4.1 documentation](#black-litterman-allocation-pyportfolioopt-1-4-1-documentation)

- [General Efficient Frontier — PyPortfolioOpt 1.5.4 documentation](#general-efficient-frontier-pyportfolioopt-1-5-4-documentation)

- [General Efficient Frontier — PyPortfolioOpt 1.4.1 documentation](#general-efficient-frontier-pyportfolioopt-1-4-1-documentation)

- [Index — PyPortfolioOpt 1.5.4 documentation](#index-pyportfolioopt-1-5-4-documentation)

- [Index — PyPortfolioOpt 1.4.1 documentation](#index-pyportfolioopt-1-4-1-documentation)

---

#

Documentation page not found

- Read the Docs Community

[pyportfolioopt.readthedocs.io](https://pyportfolioopt.readthedocs.io/)

The documentation page you requested does not exist or may have been removed.

Hosted by [](https://app.readthedocs.org/)

---

# User Guide — PyPortfolioOpt 1.4.1 documentation

* [Docs](https://pyportfolioopt.readthedocs.io/en/stable/index.html)

»

* User Guide

* [Edit on GitHub](https://github.com/robertmartin8/PyPortfolioOpt/blob/1db089602dee348f1eade9b981ca21cd35f1dcca/docs/UserGuide.rst)

* * *

User Guide[¶](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#user-guide "Permalink to this headline")

======================================================================================================================

This is designed to be a practical guide, mostly aimed at users who are interested in a quick way of optimally combining some assets (most likely stocks). However, when necessary I do introduce the required theory and also point out areas that may be suitable springboards for more advanced optimization techniques. Details about the parameters can be found in the respective documentation pages (please see the sidebar).

For this guide, we will be focusing on mean-variance optimization (MVO), which is what most people think of when they hear “portfolio optimization”. MVO forms the core of PyPortfolioOpt’s offering, though it should be noted that MVO comes in many flavours, which can have very different performance characteristics. Please refer to the sidebar to get a feeling for the possibilities, as well as the other optimization methods offered. But for now, we will continue with the standard Efficient Frontier.

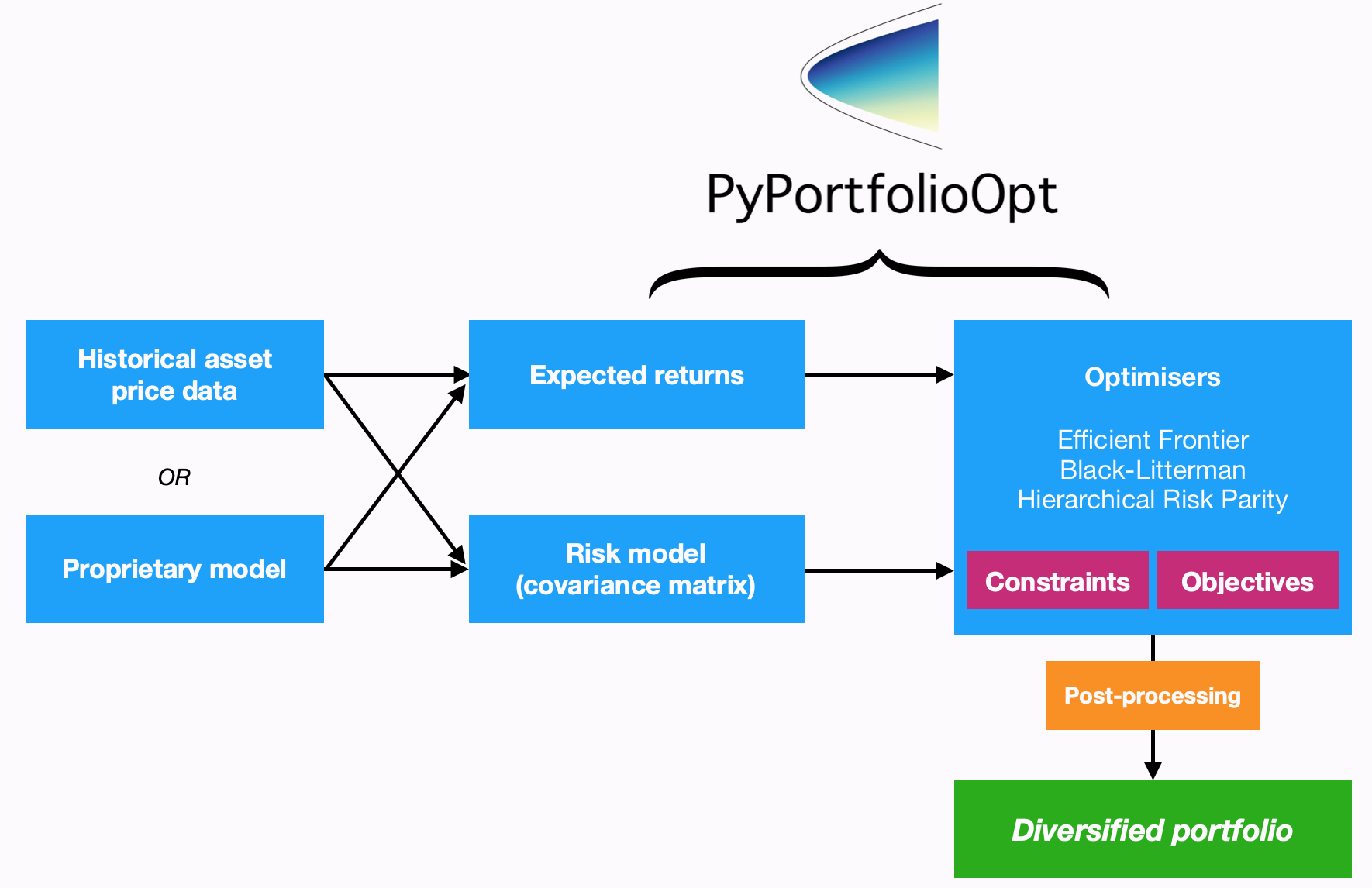

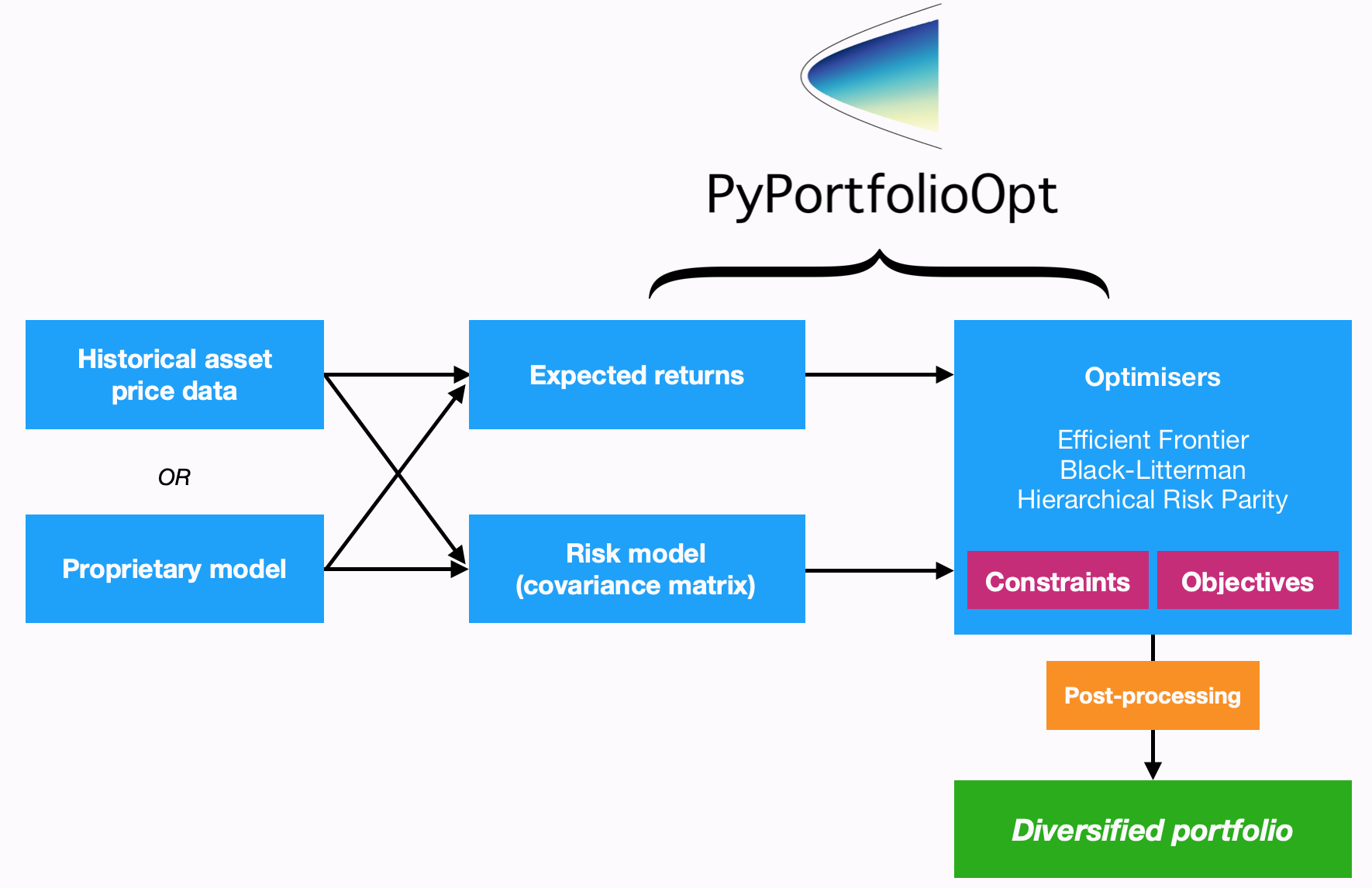

PyPortfolioOpt is designed with modularity in mind; the below flowchart sums up the current functionality and overall layout of PyPortfolioOpt.

Processing historical prices[¶](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#processing-historical-prices "Permalink to this headline")

----------------------------------------------------------------------------------------------------------------------------------------------------------

Mean-variance optimization requires two things: the expected returns of the assets, and the covariance matrix (or more generally, a _risk model_ quantifying asset risk). PyPortfolioOpt provides methods for estimating both (located in `expected_returns` and `risk_models` respectively), but also supports users who would like to use their own models.

However, I assume that most users will (at least initially) prefer to use the built-ins. In this case, all you need to supply is a dataset of historical prices for your assets. This dataset should look something like the one below:

XOM RRC BBY MA PFE JPM

date

2010\-01\-04 54.068794 51.300568 32.524055 22.062426 13.940202 35.175220

2010\-01\-05 54.279907 51.993038 33.349487 21.997149 13.741367 35.856571

2010\-01\-06 54.749043 51.690697 33.090542 22.081820 13.697187 36.053574

2010\-01\-07 54.577045 51.593170 33.616547 21.937523 13.645634 36.767757

2010\-01\-08 54.358093 52.597733 32.297466 21.945297 13.756095 36.677460

The index should consist of dates or timestamps, and each column should represent the time series of prices for an asset. A dataset of real-life stock prices has been included in the [tests folder](https://github.com/robertmartin8/PyPortfolioOpt/tree/master/tests)

of the GitHub repo.

Note

Pricing data does not have to be daily, but the frequency should be the same across all assets (workarounds exist but are not pretty).

After reading your historical prices into a pandas dataframe `df`, you need to decide between the available methods for estimating expected returns and the covariance matrix. Sensible defaults are `expected_returns.mean_historical_return()` and the Ledoit Wolf shrinkage estimate of the covariance matrix found in `risk_models.CovarianceShrinkage`. It is simply a matter of applying the relevant functions to the price dataset:

from pypfopt.expected\_returns import mean\_historical\_return

from pypfopt.risk\_models import CovarianceShrinkage

mu \= mean\_historical\_return(df)

S \= CovarianceShrinkage(df).ledoit\_wolf()

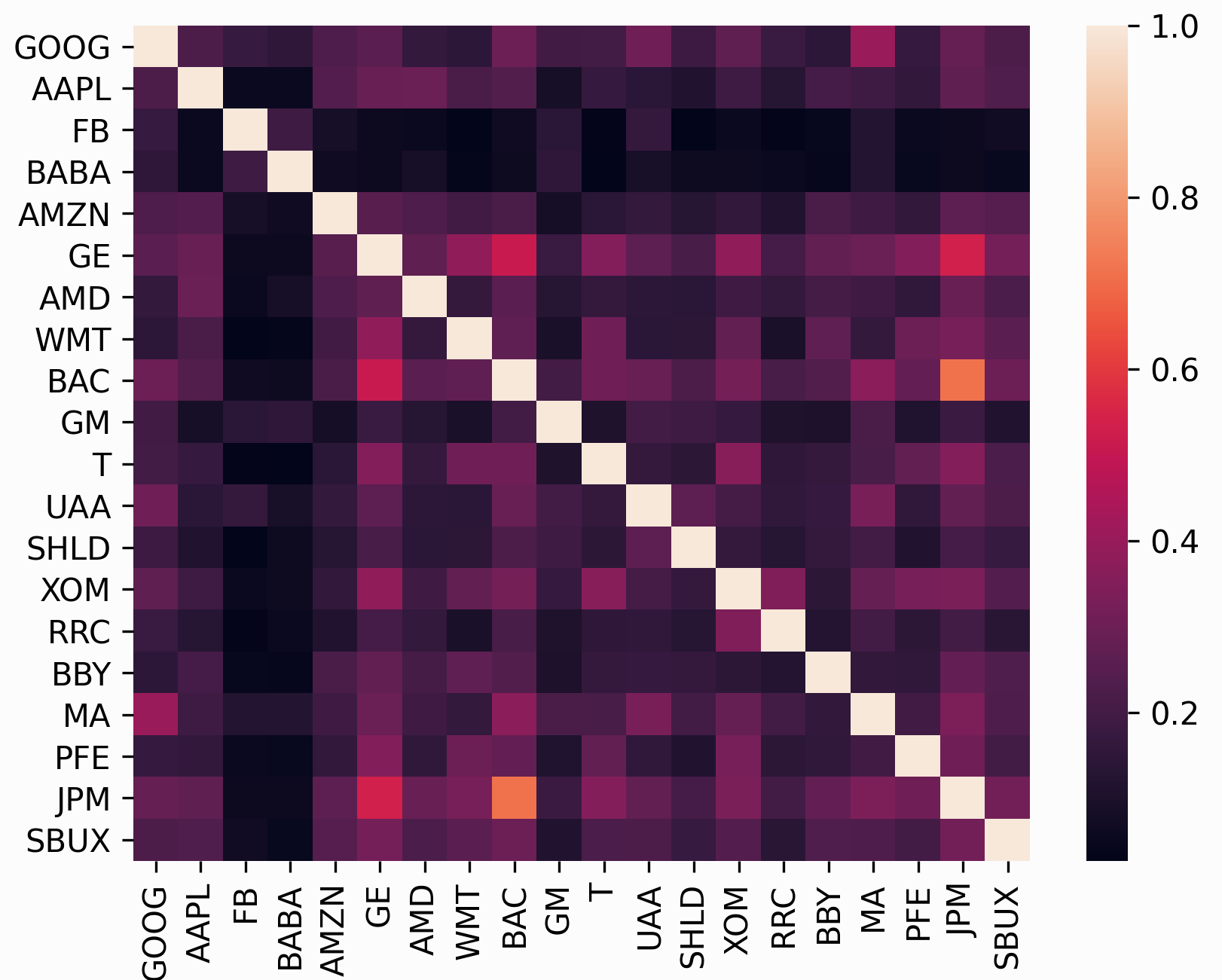

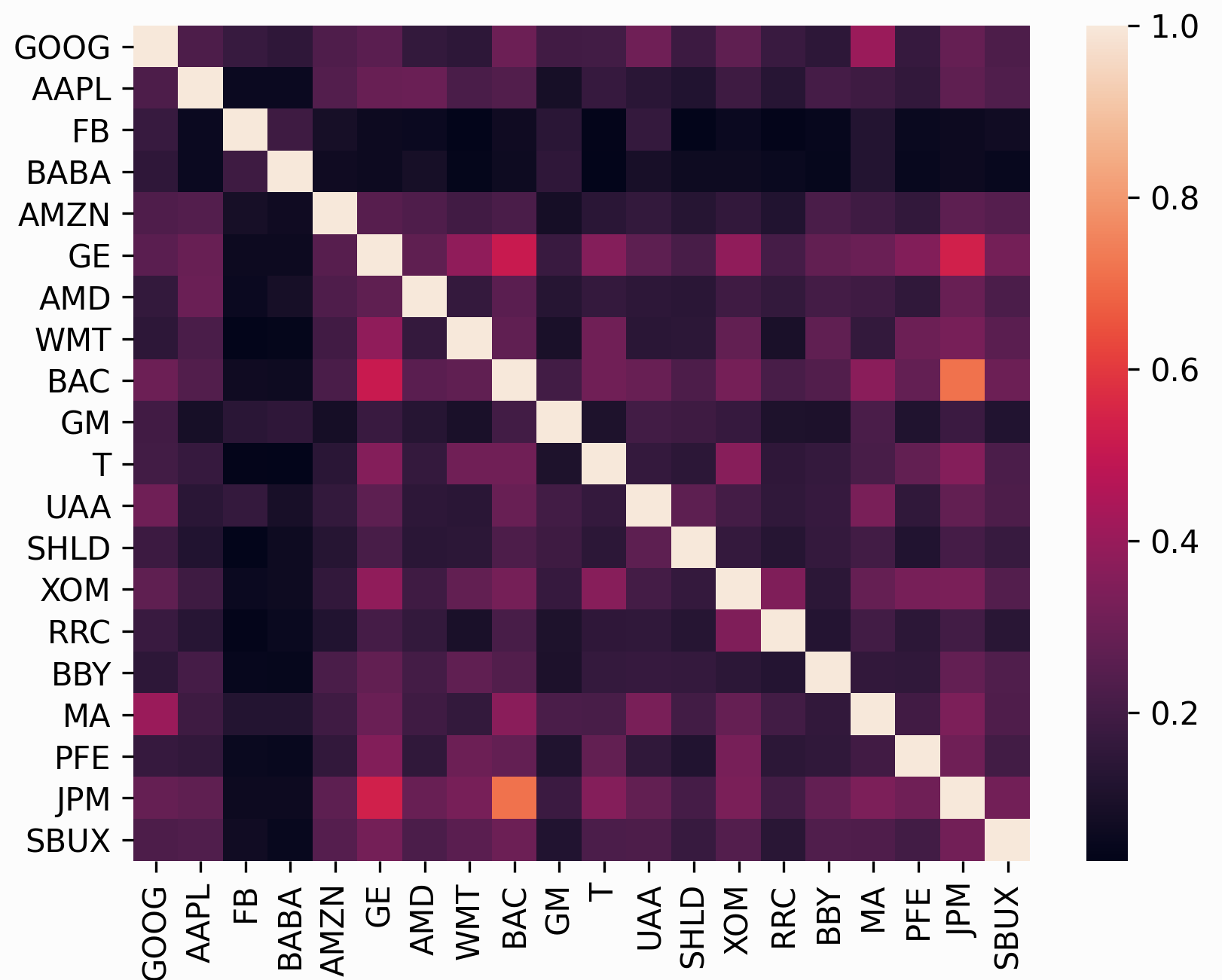

`mu` will then be a pandas series of estimated expected returns for each asset, and `S` will be the estimated covariance matrix (part of it is shown below):

GOOG AAPL FB BABA AMZN GE AMD \\

GOOG 0.045529 0.022143 0.006389 0.003720 0.026085 0.015815 0.021761

AAPL 0.022143 0.207037 0.004334 0.002954 0.058200 0.038102 0.084053

FB 0.006389 0.004334 0.029233 0.003770 0.007619 0.003008 0.005804

BABA 0.003720 0.002954 0.003770 0.013438 0.004176 0.002011 0.006332

AMZN 0.026085 0.058200 0.007619 0.004176 0.276365 0.038169 0.075657

GE 0.015815 0.038102 0.003008 0.002011 0.038169 0.083405 0.048580

AMD 0.021761 0.084053 0.005804 0.006332 0.075657 0.048580 0.388916

Now that we have expected returns and a risk model, we are ready to move on to the actual portfolio optimization.

Mean-variance optimization[¶](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#mean-variance-optimization "Permalink to this headline")

------------------------------------------------------------------------------------------------------------------------------------------------------

Mean-variance optimization is based on Harry Markowitz’s 1952 classic paper [\[1\]](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#id3)

, which spearheaded the transformation of portfolio management from an art into a science. The key insight is that by combining assets with different expected returns and volatilities, one can decide on a mathematically optimal allocation.

If \\(w\\) is the weight vector of stocks with expected returns \\(\\mu\\), then the portfolio return is equal to each stock’s weight multiplied by its return, i.e \\(w^T \\mu\\). The portfolio risk in terms of the covariance matrix \\(\\Sigma\\) is given by \\(w^T \\Sigma w\\). Portfolio optimization can then be regarded as a convex optimization problem, and a solution can be found using quadratic programming. If we denote the target return as \\(\\mu^\*\\), the precise statement of the long-only portfolio optimization problem is as follows:

\\\[\\begin{split}\\begin{equation\*} \\begin{aligned} & \\underset{w}{\\text{minimise}} & & w^T \\Sigma w \\\\ & \\text{subject to} & & w^T\\mu \\geq \\mu^\*\\\\ &&& w^T\\mathbf{1} = 1 \\\\ &&& w\_i \\geq 0 \\\\ \\end{aligned} \\end{equation\*}\\end{split}\\\]

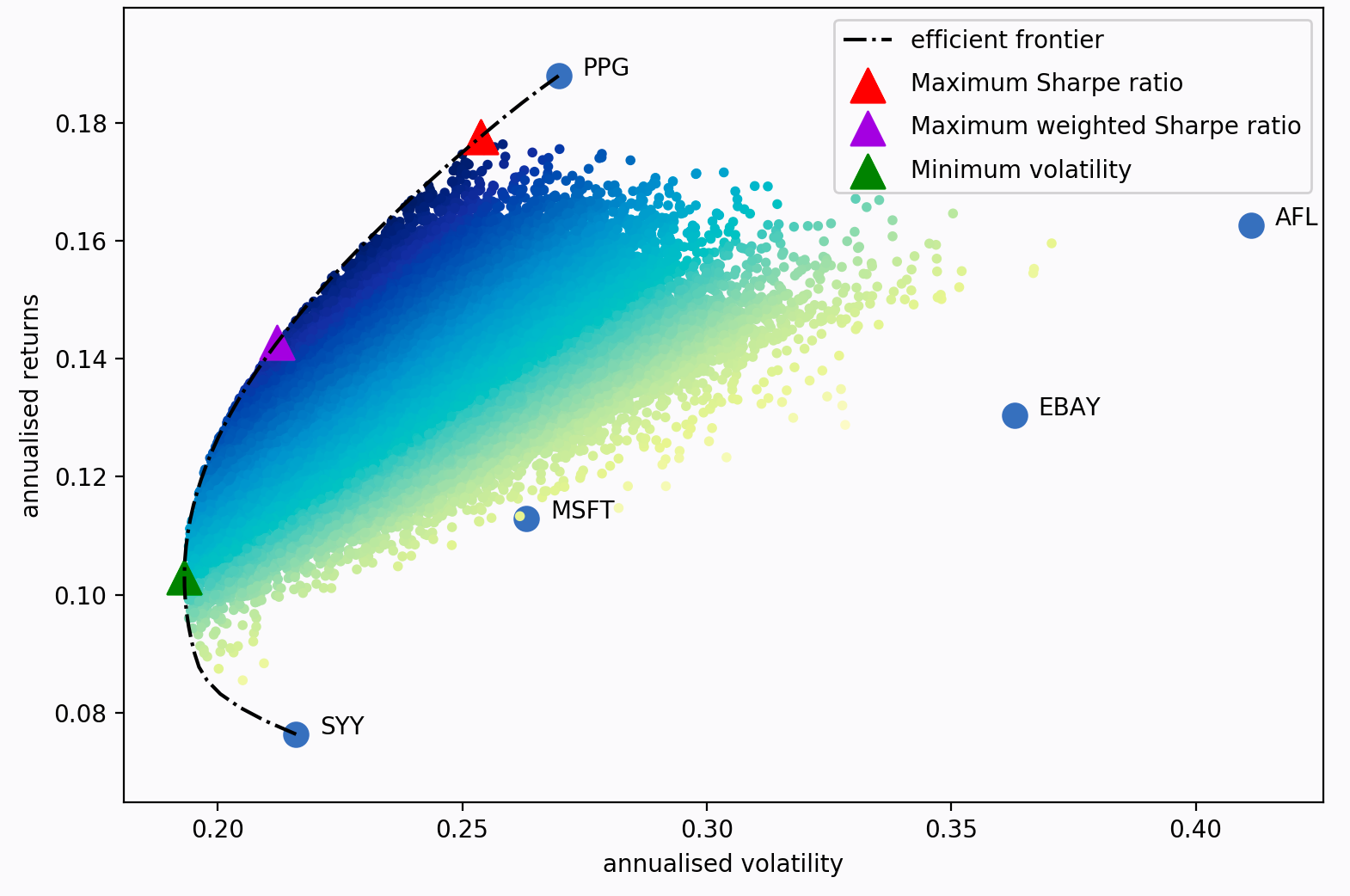

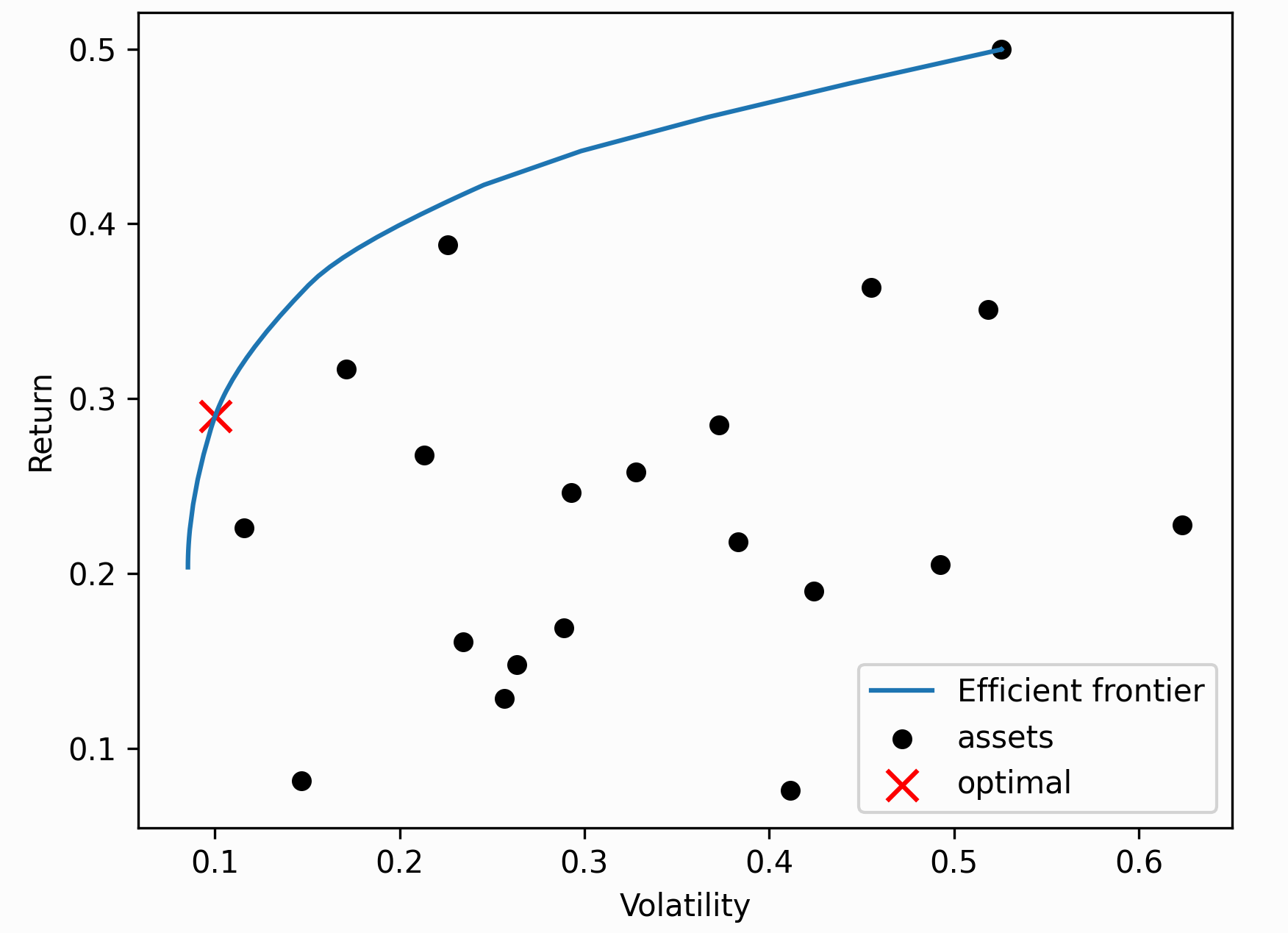

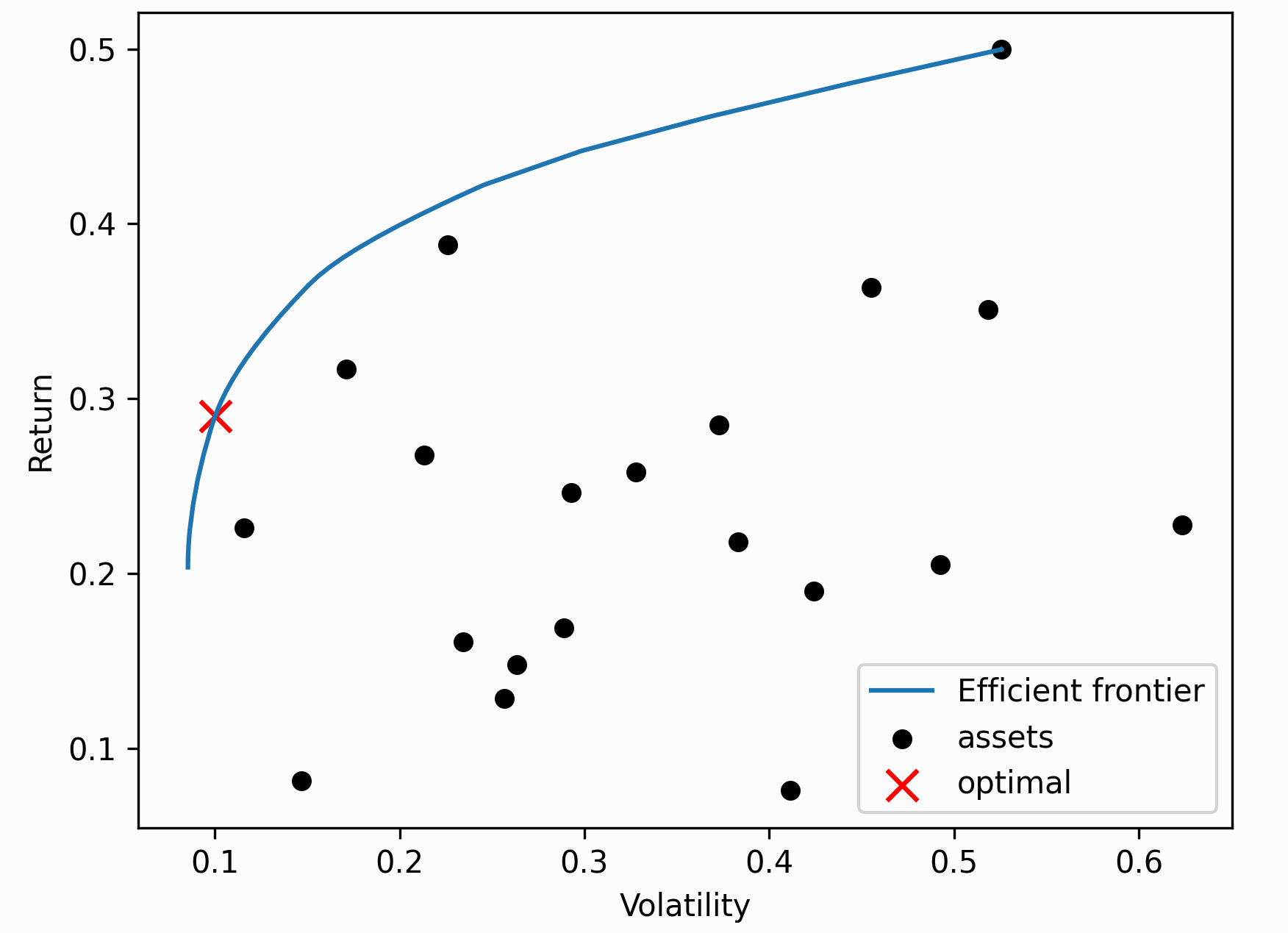

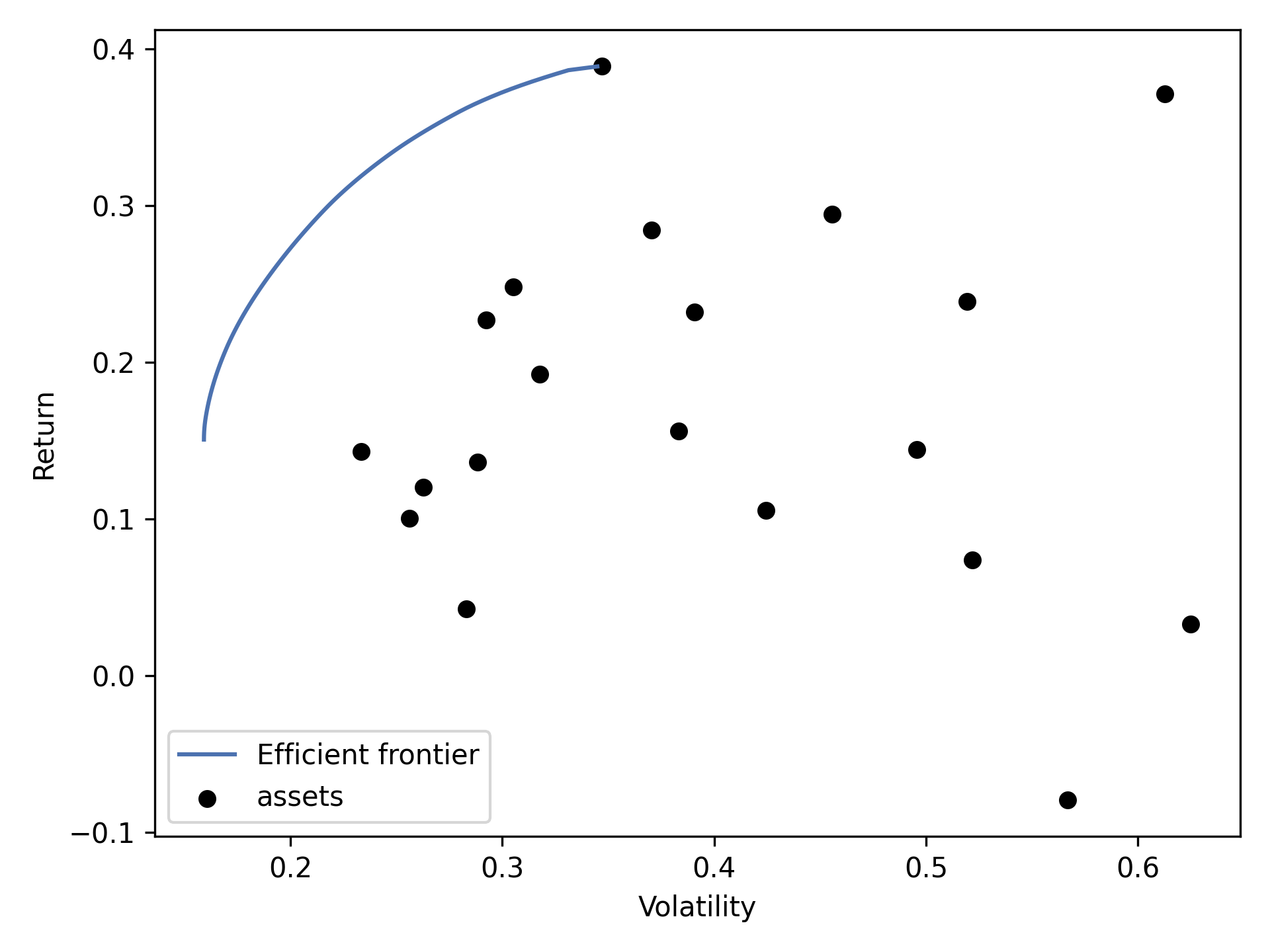

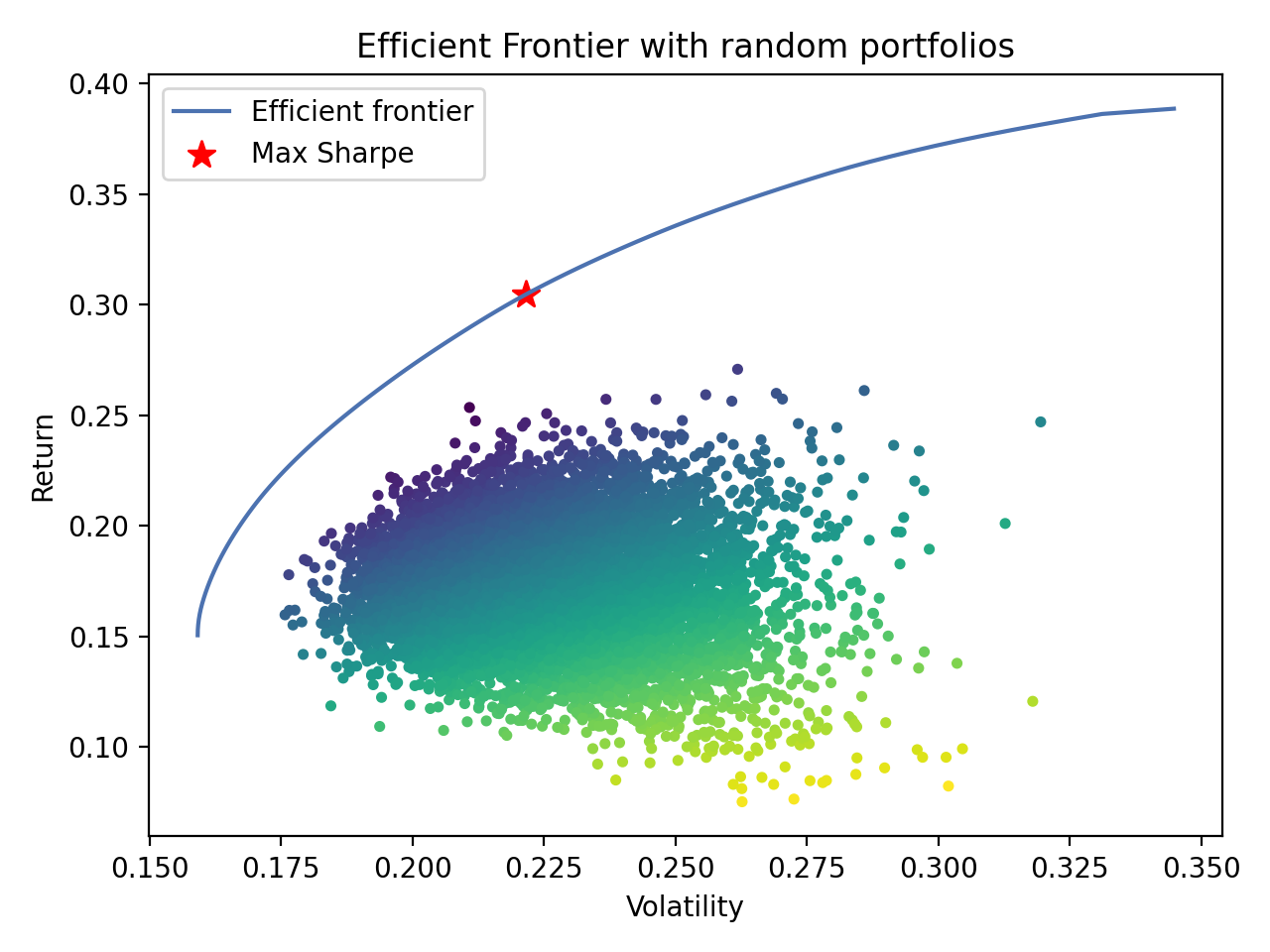

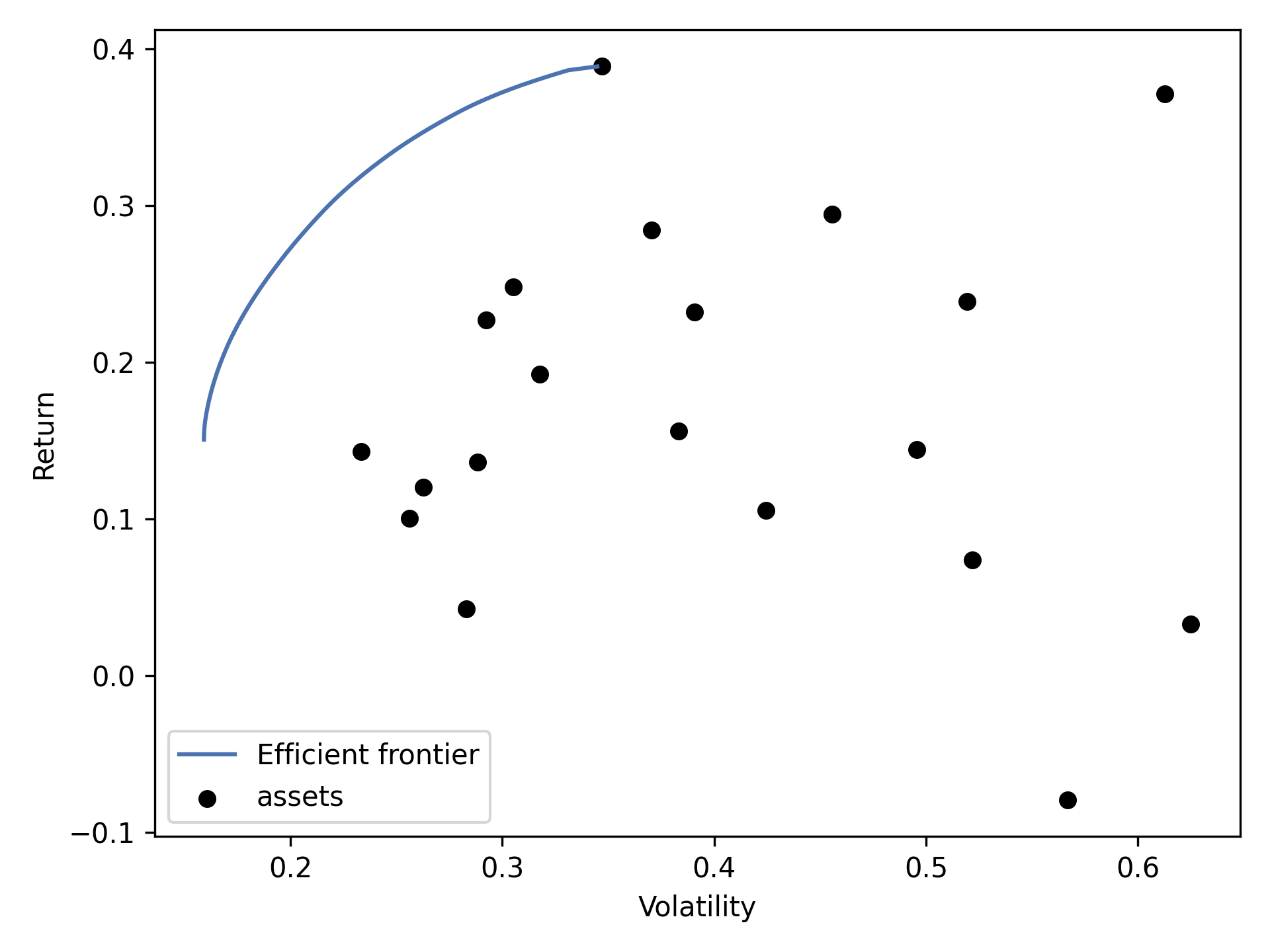

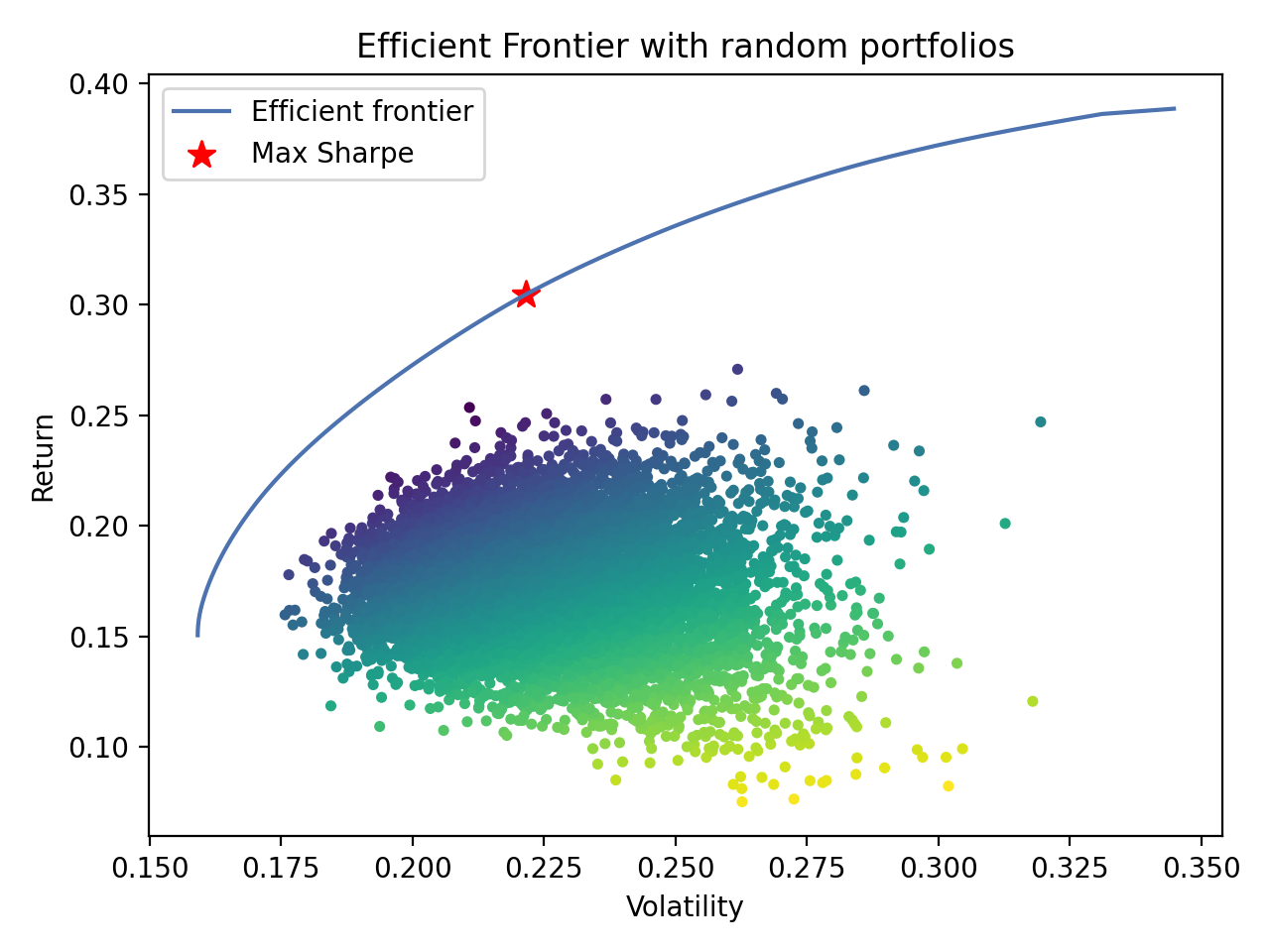

If we vary the target return, we will get a different set of weights (i.e a different portfolio) – the set of all these optimal portfolios is referred to as the **efficient frontier**.

Each dot on this diagram represents a different possible portfolio, with darker blue corresponding to ‘better’ portfolios (in terms of the Sharpe Ratio). The dotted black line is the efficient frontier itself. The triangular markers represent the best portfolios for different optimization objectives.

The Sharpe ratio is the portfolio’s return in excess of the risk-free rate, per unit risk (volatility).

\\\[SR = \\frac{R\_P - R\_f}{\\sigma}\\\]

It is particularly important because it measures the portfolio returns, adjusted for risk. So in practice, rather than trying to minimise volatility for a given target return (as per Markowitz 1952), it often makes more sense to just find the portfolio that maximises the Sharpe ratio. This is implemented as the `max_sharpe()` method in the `EfficientFrontier` class. Using the series `mu` and dataframe `S` from before:

from pypfopt.efficient\_frontier import EfficientFrontier

ef \= EfficientFrontier(mu, S)

weights \= ef.max\_sharpe()

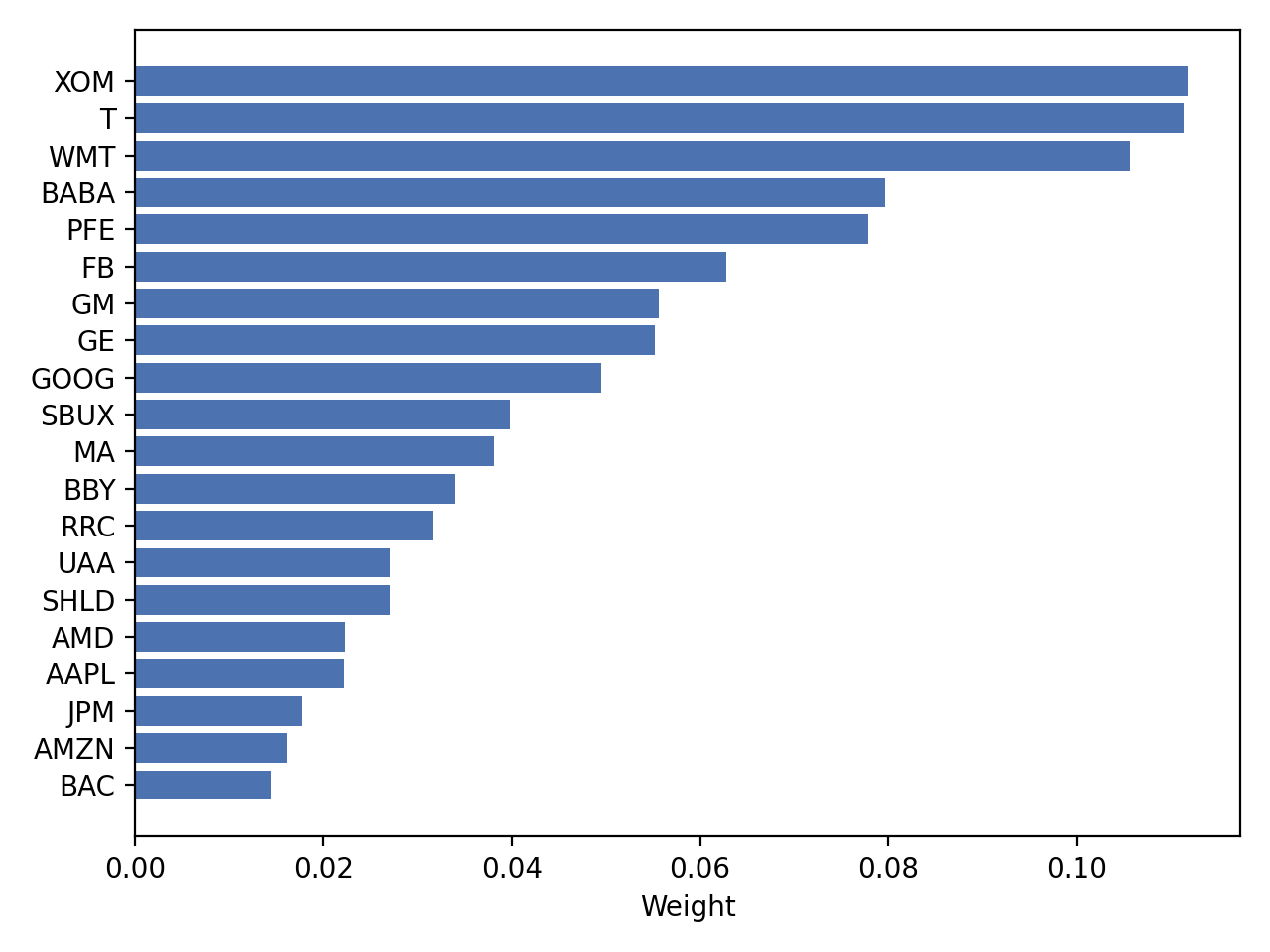

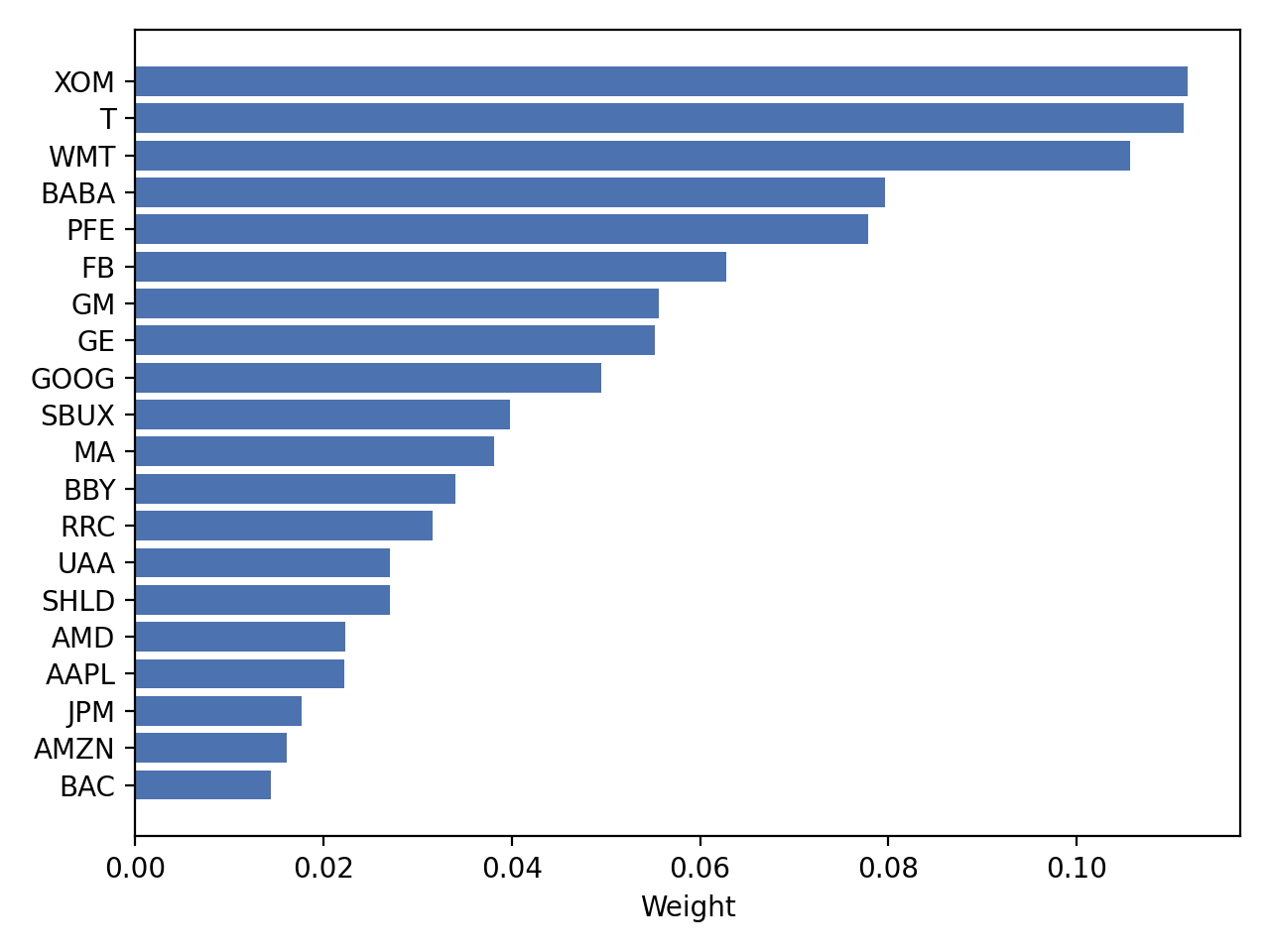

If you print these weights, you will get quite an ugly result, because they will be the raw output from the optimizer. As such, it is recommended that you use the `clean_weights()` method, which truncates tiny weights to zero and rounds the rest:

cleaned\_weights \= ef.clean\_weights()

ef.save\_weights\_to\_file("weights.txt") \# saves to file

print(cleaned\_weights)

This prints:

{'GOOG': 0.01269,

'AAPL': 0.09202,

'FB': 0.19856,

'BABA': 0.09642,

'AMZN': 0.07158,

'GE': 0.0,

'AMD': 0.0,

'WMT': 0.0,

'BAC': 0.0,

'GM': 0.0,

'T': 0.0,

'UAA': 0.0,

'SHLD': 0.0,

'XOM': 0.0,

'RRC': 0.0,

'BBY': 0.06129,

'MA': 0.24562,

'PFE': 0.18413,

'JPM': 0.0,

'SBUX': 0.03769}

If we want to know the expected performance of the portfolio with optimal weights `w`, we can use the `portfolio_performance()` method:

ef.portfolio\_performance(verbose\=True)

Expected annual return: 33.0%

Annual volatility: 21.7%

Sharpe Ratio: 1.43

A detailed discussion of optimization parameters is presented in [General Efficient Frontier](https://pyportfolioopt.readthedocs.io/en/stable/GeneralEfficientFrontier.html#efficient-frontier)

. However, there are two main variations which are discussed below.

### Short positions[¶](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#short-positions "Permalink to this headline")

To allow for shorting, simply initialise the `EfficientFrontier` object with bounds that allow negative weights, for example:

ef \= EfficientFrontier(mu, S, weight\_bounds\=(\-1,1))

This can be extended to generate **market neutral portfolios** (with weights summing to zero), but these are only available for the `efficient_risk()` and `efficient_return()` optimization methods for mathematical reasons. If you want a market neutral portfolio, pass `market_neutral=True` as shown below:

ef.efficient\_return(target\_return\=0.2, market\_neutral\=True)

### Dealing with many negligible weights[¶](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#dealing-with-many-negligible-weights "Permalink to this headline")

From experience, I have found that mean-variance optimization often sets many of the asset weights to be zero. This may not be ideal if you need to have a certain number of positions in your portfolio, for diversification purposes or otherwise.

To combat this, I have introduced an objective function which borrows the idea of regularisation from machine learning. Essentially, by adding an additional cost function to the objective, you can ‘encourage’ the optimizer to choose different weights (mathematical details are provided in the [More on L2 Regularisation](https://pyportfolioopt.readthedocs.io/en/stable/MeanVariance.html#l2-regularisation)

section). To use this feature, change the `gamma` parameter:

from pypfopt import objective\_functions

ef \= EfficientFrontier(mu, S)

ef.add\_objective(objective\_functions.L2\_reg, gamma\=0.1)

w \= ef.max\_sharpe()

print(ef.clean\_weights())

The result of this has far fewer negligible weights than before:

{'GOOG': 0.06366,

'AAPL': 0.09947,

'FB': 0.15742,

'BABA': 0.08701,

'AMZN': 0.09454,

'GE': 0.0,

'AMD': 0.0,

'WMT': 0.01766,

'BAC': 0.0,

'GM': 0.0,

'T': 0.00398,

'UAA': 0.0,

'SHLD': 0.0,

'XOM': 0.03072,

'RRC': 0.00737,

'BBY': 0.07572,

'MA': 0.1769,

'PFE': 0.12346,

'JPM': 0.0,

'SBUX': 0.06209}

### Post-processing weights[¶](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#post-processing-weights "Permalink to this headline")

In practice, we then need to convert these weights into an actual allocation, telling you how many shares of each asset you should purchase. This is discussed further in [Post-processing weights](https://pyportfolioopt.readthedocs.io/en/stable/Postprocessing.html#post-processing)

, but we provide an example below:

from pypfopt.discrete\_allocation import DiscreteAllocation, get\_latest\_prices

latest\_prices \= get\_latest\_prices(df)

da \= DiscreteAllocation(w, latest\_prices, total\_portfolio\_value\=20000)

allocation, leftover \= da.lp\_portfolio()

print(allocation)

These are the quantities of shares that should be bought to have a $20,000 portfolio:

{'AAPL': 2.0,

'FB': 12.0,

'BABA': 14.0,

'GE': 18.0,

'WMT': 40.0,

'GM': 58.0,

'T': 97.0,

'SHLD': 1.0,

'XOM': 47.0,

'RRC': 3.0,

'BBY': 1.0,

'PFE': 47.0,

'SBUX': 5.0}

Improving performance[¶](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#improving-performance "Permalink to this headline")

--------------------------------------------------------------------------------------------------------------------------------------------

Let’s say you have conducted backtests and the results aren’t spectacular. What should you try?

* Try the Hierarchical Risk Parity model (see [Other Optimizers](https://pyportfolioopt.readthedocs.io/en/stable/OtherOptimizers.html#other-optimizers)

) – which seems to robustly outperform mean-variance optimization out of sample.

* Use the Black-Litterman model to construct a more stable model of expected returns. Alternatively, just drop the expected returns altogether! There is a large body of research that suggests that minimum variance portfolios (`ef.min_volatility()`) consistently outperform maximum Sharpe ratio portfolios out-of-sample (even when measured by Sharpe ratio), because of the difficulty of forecasting expected returns.

* Try different risk models: shrinkage models are known to have better numerical properties compared with the sample covariance matrix.

* Add some new objective terms or constraints. Tune the L2 regularisation parameter to see how diversification affects the performance.

This concludes the guided tour. Head over to the appropriate sections in the sidebar to learn more about the parameters and theoretical details of the different models offered by PyPortfolioOpt. If you have any questions, please raise an issue on GitHub and I will try to respond promptly.

If you’d like even more examples, check out the cookbook [recipe](https://github.com/robertmartin8/PyPortfolioOpt/blob/master/cookbook/2-Mean-Variance-Optimization.ipynb)

.

References[¶](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#references "Permalink to this headline")

----------------------------------------------------------------------------------------------------------------------

| | |

| --- | --- |

| [\[1\]](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#id2) | Markowitz, H. (1952). [Portfolio Selection](https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1540-6261.1952.tb01525.x)

. The Journal of Finance, 7(1), 77–91. [https://doi.org/10.1111/j.1540-6261.1952.tb01525.x](https://doi.org/10.1111/j.1540-6261.1952.tb01525.x) |

---

# Expected Returns — PyPortfolioOpt 1.4.1 documentation

* [Docs](https://pyportfolioopt.readthedocs.io/en/stable/index.html)

»

* Expected Returns

* [Edit on GitHub](https://github.com/robertmartin8/PyPortfolioOpt/blob/1db089602dee348f1eade9b981ca21cd35f1dcca/docs/ExpectedReturns.rst)

* * *

Expected Returns[¶](https://pyportfolioopt.readthedocs.io/en/stable/ExpectedReturns.html#expected-returns "Permalink to this headline")

========================================================================================================================================

Mean-variance optimization requires knowledge of the expected returns. In practice, these are rather difficult to know with any certainty. Thus the best we can do is to come up with estimates, for example by extrapolating historical data, This is the main flaw in mean-variance optimization – the optimization procedure is sound, and provides strong mathematical guarantees, _given the correct inputs_. This is one of the reasons why I have emphasised modularity: users should be able to come up with their own superior models and feed them into the optimizer.

Caution

Supplying expected returns can do more harm than good. If predicting stock returns were as easy as calculating the mean historical return, we’d all be rich! For most use-cases, I would suggest that you focus your efforts on choosing an appropriate risk model (see [Risk Models](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#risk-models)

).

As of v0.5.0, you can use [Black-Litterman Allocation](https://pyportfolioopt.readthedocs.io/en/stable/BlackLitterman.html#black-litterman)

to significantly improve the quality of your estimate of the expected returns.

The `expected_returns` module provides functions for estimating the expected returns of the assets, which is a required input in mean-variance optimization.

By convention, the output of these methods is expected _annual_ returns. It is assumed that _daily_ prices are provided, though in reality the functions are agnostic to the time period (just change the `frequency` parameter). Asset prices must be given as a pandas dataframe, as per the format described in the [User Guide](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#user-guide)

.

All of the functions process the price data into percentage returns data, before calculating their respective estimates of expected returns.

Currently implemented:

> * general return model function, allowing you to run any return model from one function.

> * mean historical return

> * exponentially weighted mean historical return

> * CAPM estimate of returns

Additionally, we provide utility functions to convert from returns to prices and vice-versa.

Note

For any of these methods, if you would prefer to pass returns (the default is prices), set the boolean flag `returns_data=True`

`pypfopt.expected_returns.``mean_historical_return`(_prices_, _returns\_data=False_, _compounding=True_, _frequency=252_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/expected_returns.html#mean_historical_return)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/ExpectedReturns.html#pypfopt.expected_returns.mean_historical_return "Permalink to this definition")

Calculate annualised mean (daily) historical return from input (daily) asset prices. Use `compounding` to toggle between the default geometric mean (CAGR) and the arithmetic mean.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices. These **should not** be log returns.

* **compounding** (_bool__,_ _defaults to True_) – computes geometric mean returns if True, arithmetic otherwise, optional.

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year) |

| Returns: | annualised mean (daily) return for each asset |

| Return type: | pd.Series |

This is probably the default textbook approach. It is intuitive and easily interpretable, however the estimates are subject to large uncertainty. This is a problem especially in the context of a mean-variance optimizer, which will maximise the erroneous inputs.

`pypfopt.expected_returns.``ema_historical_return`(_prices_, _returns\_data=False_, _compounding=True_, _span=500_, _frequency=252_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/expected_returns.html#ema_historical_return)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/ExpectedReturns.html#pypfopt.expected_returns.ema_historical_return "Permalink to this definition")

Calculate the exponentially-weighted mean of (daily) historical returns, giving higher weight to more recent data.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices. These **should not** be log returns.

* **compounding** (_bool__,_ _defaults to True_) – computes geometric mean returns if True, arithmetic otherwise, optional.

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year)

* **span** (_int__,_ _optional_) – the time-span for the EMA, defaults to 500-day EMA. |

| Returns: | annualised exponentially-weighted mean (daily) return of each asset |

| Return type: | pd.Series |

The exponential moving average is a simple improvement over the mean historical return; it gives more credence to recent returns and thus aims to increase the relevance of the estimates. This is parameterised by the `span` parameter, which gives users the ability to decide exactly how much more weight is given to recent data. Generally, I would err on the side of a higher span – in the limit, this tends towards the mean historical return. However, if you plan on rebalancing much more frequently, there is a case to be made for lowering the span in order to capture recent trends.

`pypfopt.expected_returns.``capm_return`(_prices_, _market\_prices=None_, _returns\_data=False_, _risk\_free\_rate=0.02_, _compounding=True_, _frequency=252_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/expected_returns.html#capm_return)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/ExpectedReturns.html#pypfopt.expected_returns.capm_return "Permalink to this definition")

Compute a return estimate using the Capital Asset Pricing Model. Under the CAPM, asset returns are equal to market returns plus a \\(�eta\\) term encoding the relative risk of the asset.

\\\[R\_i = R\_f + \\beta\_i (E(R\_m) - R\_f)\\\]

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **market\_prices** (_pd.DataFrame__,_ _optional_) – adjusted closing prices of the benchmark, defaults to None

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first arguments are returns instead of prices.

* **risk\_free\_rate** (_float__,_ _optional_) – risk-free rate of borrowing/lending, defaults to 0.02. You should use the appropriate time period, corresponding to the frequency parameter.

* **compounding** (_bool__,_ _defaults to True_) – computes geometric mean returns if True, arithmetic otherwise, optional.

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year) |

| Returns: | annualised return estimate |

| Return type: | pd.Series |

`pypfopt.expected_returns.``returns_from_prices`(_prices_, _log\_returns=False_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/expected_returns.html#returns_from_prices)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/ExpectedReturns.html#pypfopt.expected_returns.returns_from_prices "Permalink to this definition")

Calculate the returns given prices.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted (daily) closing prices of the asset, each row is a date and each column is a ticker/id.

* **log\_returns** (_bool__,_ _defaults to False_) – whether to compute using log returns |

| Returns: | (daily) returns |

| Return type: | pd.DataFrame |

`pypfopt.expected_returns.``prices_from_returns`(_returns_, _log\_returns=False_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/expected_returns.html#prices_from_returns)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/ExpectedReturns.html#pypfopt.expected_returns.prices_from_returns "Permalink to this definition")

Calculate the pseudo-prices given returns. These are not true prices because the initial prices are all set to 1, but it behaves as intended when passed to any PyPortfolioOpt method.

| | |

| --- | --- |

| Parameters: | * **returns** (_pd.DataFrame_) – (daily) percentage returns of the assets

* **log\_returns** (_bool__,_ _defaults to False_) – whether to compute using log returns |

| Returns: | (daily) pseudo-prices. |

| Return type: | pd.DataFrame |

---

# User Guide — PyPortfolioOpt 1.5.4 documentation

* [Docs](https://pyportfolioopt.readthedocs.io/en/latest/index.html)

»

* User Guide

* [Edit on GitHub](https://github.com/robertmartin8/PyPortfolioOpt/blob/master/docs/UserGuide.rst)

* * *

User Guide[¶](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#user-guide "Permalink to this headline")

======================================================================================================================

This is designed to be a practical guide, mostly aimed at users who are interested in a quick way of optimally combining some assets (most likely stocks). However, when necessary I do introduce the required theory and also point out areas that may be suitable springboards for more advanced optimization techniques. Details about the parameters can be found in the respective documentation pages (please see the sidebar).

For this guide, we will be focusing on mean-variance optimization (MVO), which is what most people think of when they hear “portfolio optimization”. MVO forms the core of PyPortfolioOpt’s offering, though it should be noted that MVO comes in many flavours, which can have very different performance characteristics. Please refer to the sidebar to get a feeling for the possibilities, as well as the other optimization methods offered. But for now, we will continue with the standard Efficient Frontier.

PyPortfolioOpt is designed with modularity in mind; the below flowchart sums up the current functionality and overall layout of PyPortfolioOpt.

Processing historical prices[¶](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#processing-historical-prices "Permalink to this headline")

----------------------------------------------------------------------------------------------------------------------------------------------------------

Mean-variance optimization requires two things: the expected returns of the assets, and the covariance matrix (or more generally, a _risk model_ quantifying asset risk). PyPortfolioOpt provides methods for estimating both (located in `expected_returns` and `risk_models` respectively), but also supports users who would like to use their own models.

However, I assume that most users will (at least initially) prefer to use the built-ins. In this case, all you need to supply is a dataset of historical prices for your assets. This dataset should look something like the one below:

XOM RRC BBY MA PFE JPM

date

2010\-01\-04 54.068794 51.300568 32.524055 22.062426 13.940202 35.175220

2010\-01\-05 54.279907 51.993038 33.349487 21.997149 13.741367 35.856571

2010\-01\-06 54.749043 51.690697 33.090542 22.081820 13.697187 36.053574

2010\-01\-07 54.577045 51.593170 33.616547 21.937523 13.645634 36.767757

2010\-01\-08 54.358093 52.597733 32.297466 21.945297 13.756095 36.677460

The index should consist of dates or timestamps, and each column should represent the time series of prices for an asset. A dataset of real-life stock prices has been included in the [tests folder](https://github.com/robertmartin8/PyPortfolioOpt/tree/master/tests)

of the GitHub repo.

Note

Pricing data does not have to be daily, but the frequency should be the same across all assets (workarounds exist but are not pretty).

After reading your historical prices into a pandas dataframe `df`, you need to decide between the available methods for estimating expected returns and the covariance matrix. Sensible defaults are `expected_returns.mean_historical_return()` and the Ledoit Wolf shrinkage estimate of the covariance matrix found in `risk_models.CovarianceShrinkage`. It is simply a matter of applying the relevant functions to the price dataset:

from pypfopt.expected\_returns import mean\_historical\_return

from pypfopt.risk\_models import CovarianceShrinkage

mu \= mean\_historical\_return(df)

S \= CovarianceShrinkage(df).ledoit\_wolf()

`mu` will then be a pandas series of estimated expected returns for each asset, and `S` will be the estimated covariance matrix (part of it is shown below):

GOOG AAPL FB BABA AMZN GE AMD \\

GOOG 0.045529 0.022143 0.006389 0.003720 0.026085 0.015815 0.021761

AAPL 0.022143 0.207037 0.004334 0.002954 0.058200 0.038102 0.084053

FB 0.006389 0.004334 0.029233 0.003770 0.007619 0.003008 0.005804

BABA 0.003720 0.002954 0.003770 0.013438 0.004176 0.002011 0.006332

AMZN 0.026085 0.058200 0.007619 0.004176 0.276365 0.038169 0.075657

GE 0.015815 0.038102 0.003008 0.002011 0.038169 0.083405 0.048580

AMD 0.021761 0.084053 0.005804 0.006332 0.075657 0.048580 0.388916

Now that we have expected returns and a risk model, we are ready to move on to the actual portfolio optimization.

Mean-variance optimization[¶](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#mean-variance-optimization "Permalink to this headline")

------------------------------------------------------------------------------------------------------------------------------------------------------

Mean-variance optimization is based on Harry Markowitz’s 1952 classic paper [\[1\]](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#id3)

, which spearheaded the transformation of portfolio management from an art into a science. The key insight is that by combining assets with different expected returns and volatilities, one can decide on a mathematically optimal allocation.

If \\(w\\) is the weight vector of stocks with expected returns \\(\\mu\\), then the portfolio return is equal to each stock’s weight multiplied by its return, i.e \\(w^T \\mu\\). The portfolio risk in terms of the covariance matrix \\(\\Sigma\\) is given by \\(w^T \\Sigma w\\). Portfolio optimization can then be regarded as a convex optimization problem, and a solution can be found using quadratic programming. If we denote the target return as \\(\\mu^\*\\), the precise statement of the long-only portfolio optimization problem is as follows:

\\\[\\begin{split}\\begin{equation\*} \\begin{aligned} & \\underset{w}{\\text{minimise}} & & w^T \\Sigma w \\\\ & \\text{subject to} & & w^T\\mu \\geq \\mu^\*\\\\ &&& w^T\\mathbf{1} = 1 \\\\ &&& w\_i \\geq 0 \\\\ \\end{aligned} \\end{equation\*}\\end{split}\\\]

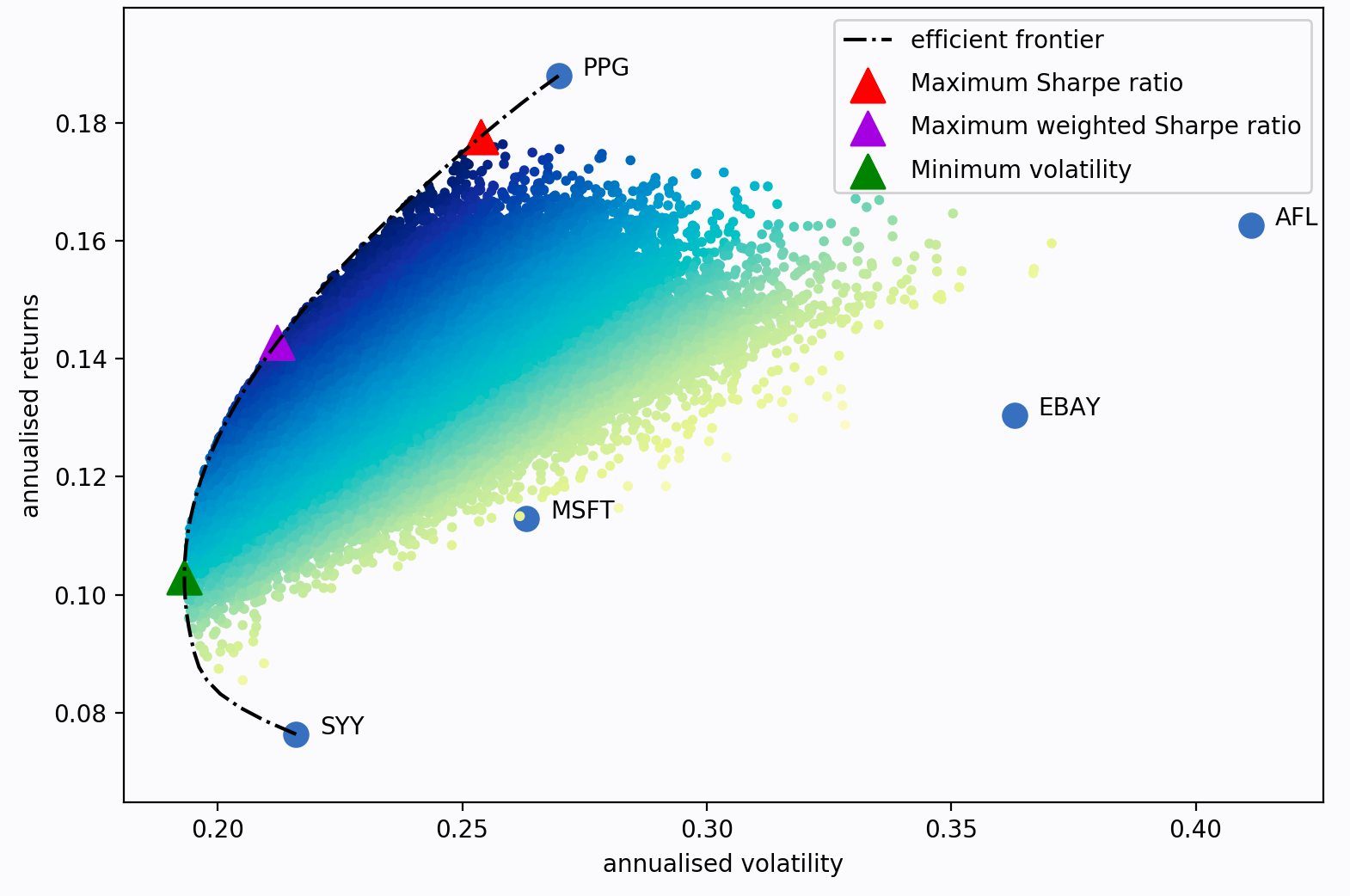

If we vary the target return, we will get a different set of weights (i.e a different portfolio) – the set of all these optimal portfolios is referred to as the **efficient frontier**.

Each dot on this diagram represents a different possible portfolio, with darker blue corresponding to ‘better’ portfolios (in terms of the Sharpe Ratio). The dotted black line is the efficient frontier itself. The triangular markers represent the best portfolios for different optimization objectives.

The Sharpe ratio is the portfolio’s return in excess of the risk-free rate, per unit risk (volatility).

\\\[SR = \\frac{R\_P - R\_f}{\\sigma}\\\]

It is particularly important because it measures the portfolio returns, adjusted for risk. So in practice, rather than trying to minimise volatility for a given target return (as per Markowitz 1952), it often makes more sense to just find the portfolio that maximises the Sharpe ratio. This is implemented as the `max_sharpe()` method in the `EfficientFrontier` class. Using the series `mu` and dataframe `S` from before:

from pypfopt.efficient\_frontier import EfficientFrontier

ef \= EfficientFrontier(mu, S)

weights \= ef.max\_sharpe()

If you print these weights, you will get quite an ugly result, because they will be the raw output from the optimizer. As such, it is recommended that you use the `clean_weights()` method, which truncates tiny weights to zero and rounds the rest:

cleaned\_weights \= ef.clean\_weights()

ef.save\_weights\_to\_file("weights.txt") \# saves to file

print(cleaned\_weights)

This prints:

{'GOOG': 0.01269,

'AAPL': 0.09202,

'FB': 0.19856,

'BABA': 0.09642,

'AMZN': 0.07158,

'GE': 0.0,

'AMD': 0.0,

'WMT': 0.0,

'BAC': 0.0,

'GM': 0.0,

'T': 0.0,

'UAA': 0.0,

'SHLD': 0.0,

'XOM': 0.0,

'RRC': 0.0,

'BBY': 0.06129,

'MA': 0.24562,

'PFE': 0.18413,

'JPM': 0.0,

'SBUX': 0.03769}

If we want to know the expected performance of the portfolio with optimal weights `w`, we can use the `portfolio_performance()` method:

ef.portfolio\_performance(verbose\=True)

Expected annual return: 33.0%

Annual volatility: 21.7%

Sharpe Ratio: 1.43

A detailed discussion of optimization parameters is presented in [General Efficient Frontier](https://pyportfolioopt.readthedocs.io/en/latest/GeneralEfficientFrontier.html#efficient-frontier)

. However, there are two main variations which are discussed below.

### Short positions[¶](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#short-positions "Permalink to this headline")

To allow for shorting, simply initialise the `EfficientFrontier` object with bounds that allow negative weights, for example:

ef \= EfficientFrontier(mu, S, weight\_bounds\=(\-1,1))

This can be extended to generate **market neutral portfolios** (with weights summing to zero), but these are only available for the `efficient_risk()` and `efficient_return()` optimization methods for mathematical reasons. If you want a market neutral portfolio, pass `market_neutral=True` as shown below:

ef.efficient\_return(target\_return\=0.2, market\_neutral\=True)

### Dealing with many negligible weights[¶](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#dealing-with-many-negligible-weights "Permalink to this headline")

From experience, I have found that mean-variance optimization often sets many of the asset weights to be zero. This may not be ideal if you need to have a certain number of positions in your portfolio, for diversification purposes or otherwise.

To combat this, I have introduced an objective function which borrows the idea of regularisation from machine learning. Essentially, by adding an additional cost function to the objective, you can ‘encourage’ the optimizer to choose different weights (mathematical details are provided in the [More on L2 Regularisation](https://pyportfolioopt.readthedocs.io/en/latest/MeanVariance.html#l2-regularisation)

section). To use this feature, change the `gamma` parameter:

from pypfopt import objective\_functions

ef \= EfficientFrontier(mu, S)

ef.add\_objective(objective\_functions.L2\_reg, gamma\=0.1)

w \= ef.max\_sharpe()

print(ef.clean\_weights())

The result of this has far fewer negligible weights than before:

{'GOOG': 0.06366,

'AAPL': 0.09947,

'FB': 0.15742,

'BABA': 0.08701,

'AMZN': 0.09454,

'GE': 0.0,

'AMD': 0.0,

'WMT': 0.01766,

'BAC': 0.0,

'GM': 0.0,

'T': 0.00398,

'UAA': 0.0,

'SHLD': 0.0,

'XOM': 0.03072,

'RRC': 0.00737,

'BBY': 0.07572,

'MA': 0.1769,

'PFE': 0.12346,

'JPM': 0.0,

'SBUX': 0.06209}

### Post-processing weights[¶](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#post-processing-weights "Permalink to this headline")

In practice, we then need to convert these weights into an actual allocation, telling you how many shares of each asset you should purchase. This is discussed further in [Post-processing weights](https://pyportfolioopt.readthedocs.io/en/latest/Postprocessing.html#post-processing)

, but we provide an example below:

from pypfopt.discrete\_allocation import DiscreteAllocation, get\_latest\_prices

latest\_prices \= get\_latest\_prices(df)

da \= DiscreteAllocation(w, latest\_prices, total\_portfolio\_value\=20000)

allocation, leftover \= da.lp\_portfolio()

print(allocation)

These are the quantities of shares that should be bought to have a $20,000 portfolio:

{'AAPL': 2.0,

'FB': 12.0,

'BABA': 14.0,

'GE': 18.0,

'WMT': 40.0,

'GM': 58.0,

'T': 97.0,

'SHLD': 1.0,

'XOM': 47.0,

'RRC': 3.0,

'BBY': 1.0,

'PFE': 47.0,

'SBUX': 5.0}

Improving performance[¶](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#improving-performance "Permalink to this headline")

--------------------------------------------------------------------------------------------------------------------------------------------

Let’s say you have conducted backtests and the results aren’t spectacular. What should you try?

* Try the Hierarchical Risk Parity model (see [Other Optimizers](https://pyportfolioopt.readthedocs.io/en/latest/OtherOptimizers.html#other-optimizers)

) – which seems to robustly outperform mean-variance optimization out of sample.

* Use the Black-Litterman model to construct a more stable model of expected returns. Alternatively, just drop the expected returns altogether! There is a large body of research that suggests that minimum variance portfolios (`ef.min_volatility()`) consistently outperform maximum Sharpe ratio portfolios out-of-sample (even when measured by Sharpe ratio), because of the difficulty of forecasting expected returns.

* Try different risk models: shrinkage models are known to have better numerical properties compared with the sample covariance matrix.

* Add some new objective terms or constraints. Tune the L2 regularisation parameter to see how diversification affects the performance.

This concludes the guided tour. Head over to the appropriate sections in the sidebar to learn more about the parameters and theoretical details of the different models offered by PyPortfolioOpt. If you have any questions, please raise an issue on GitHub and I will try to respond promptly.

If you’d like even more examples, check out the cookbook [recipe](https://github.com/robertmartin8/PyPortfolioOpt/blob/master/cookbook/2-Mean-Variance-Optimization.ipynb)

.

References[¶](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#references "Permalink to this headline")

----------------------------------------------------------------------------------------------------------------------

| | |

| --- | --- |

| [\[1\]](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#id2) | Markowitz, H. (1952). [Portfolio Selection](https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1540-6261.1952.tb01525.x)

. The Journal of Finance, 7(1), 77–91. [https://doi.org/10.1111/j.1540-6261.1952.tb01525.x](https://doi.org/10.1111/j.1540-6261.1952.tb01525.x) |

---

# Expected Returns — PyPortfolioOpt 1.5.4 documentation

* [Docs](https://pyportfolioopt.readthedocs.io/en/latest/index.html)

»

* Expected Returns

* [Edit on GitHub](https://github.com/robertmartin8/PyPortfolioOpt/blob/master/docs/ExpectedReturns.rst)

* * *

Expected Returns[¶](https://pyportfolioopt.readthedocs.io/en/latest/ExpectedReturns.html#expected-returns "Permalink to this headline")

========================================================================================================================================

Mean-variance optimization requires knowledge of the expected returns. In practice, these are rather difficult to know with any certainty. Thus the best we can do is to come up with estimates, for example by extrapolating historical data, This is the main flaw in mean-variance optimization – the optimization procedure is sound, and provides strong mathematical guarantees, _given the correct inputs_. This is one of the reasons why I have emphasised modularity: users should be able to come up with their own superior models and feed them into the optimizer.

Caution

Supplying expected returns can do more harm than good. If predicting stock returns were as easy as calculating the mean historical return, we’d all be rich! For most use-cases, I would suggest that you focus your efforts on choosing an appropriate risk model (see [Risk Models](https://pyportfolioopt.readthedocs.io/en/latest/RiskModels.html#risk-models)

).

As of v0.5.0, you can use [Black-Litterman Allocation](https://pyportfolioopt.readthedocs.io/en/latest/BlackLitterman.html#black-litterman)

to significantly improve the quality of your estimate of the expected returns.

The `expected_returns` module provides functions for estimating the expected returns of the assets, which is a required input in mean-variance optimization.

By convention, the output of these methods is expected _annual_ returns. It is assumed that _daily_ prices are provided, though in reality the functions are agnostic to the time period (just change the `frequency` parameter). Asset prices must be given as a pandas dataframe, as per the format described in the [User Guide](https://pyportfolioopt.readthedocs.io/en/latest/UserGuide.html#user-guide)

.

All of the functions process the price data into percentage returns data, before calculating their respective estimates of expected returns.

Currently implemented:

> * general return model function, allowing you to run any return model from one function.

> * mean historical return

> * exponentially weighted mean historical return

> * CAPM estimate of returns

Additionally, we provide utility functions to convert from returns to prices and vice-versa.

Note

For any of these methods, if you would prefer to pass returns (the default is prices), set the boolean flag `returns_data=True`

`pypfopt.expected_returns.``mean_historical_return`(_prices_, _returns\_data=False_, _compounding=True_, _frequency=252_, _log\_returns=False_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/latest/_modules/pypfopt/expected_returns.html#mean_historical_return)

[¶](https://pyportfolioopt.readthedocs.io/en/latest/ExpectedReturns.html#pypfopt.expected_returns.mean_historical_return "Permalink to this definition")

Calculate annualised mean (daily) historical return from input (daily) asset prices. Use `compounding` to toggle between the default geometric mean (CAGR) and the arithmetic mean.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices. These **should not** be log returns.

* **compounding** (_bool__,_ _defaults to True_) – computes geometric mean returns if True, arithmetic otherwise, optional.

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year)

* **log\_returns** (_bool__,_ _defaults to False_) – whether to compute using log returns |

| Returns: | annualised mean (daily) return for each asset |

| Return type: | pd.Series |

This is probably the default textbook approach. It is intuitive and easily interpretable, however the estimates are subject to large uncertainty. This is a problem especially in the context of a mean-variance optimizer, which will maximise the erroneous inputs.

`pypfopt.expected_returns.``ema_historical_return`(_prices_, _returns\_data=False_, _compounding=True_, _span=500_, _frequency=252_, _log\_returns=False_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/latest/_modules/pypfopt/expected_returns.html#ema_historical_return)

[¶](https://pyportfolioopt.readthedocs.io/en/latest/ExpectedReturns.html#pypfopt.expected_returns.ema_historical_return "Permalink to this definition")

Calculate the exponentially-weighted mean of (daily) historical returns, giving higher weight to more recent data.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices. These **should not** be log returns.

* **compounding** (_bool__,_ _defaults to True_) – computes geometric mean returns if True, arithmetic otherwise, optional.

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year)

* **span** (_int__,_ _optional_) – the time-span for the EMA, defaults to 500-day EMA.

* **log\_returns** (_bool__,_ _defaults to False_) – whether to compute using log returns |

| Returns: | annualised exponentially-weighted mean (daily) return of each asset |

| Return type: | pd.Series |

The exponential moving average is a simple improvement over the mean historical return; it gives more credence to recent returns and thus aims to increase the relevance of the estimates. This is parameterised by the `span` parameter, which gives users the ability to decide exactly how much more weight is given to recent data. Generally, I would err on the side of a higher span – in the limit, this tends towards the mean historical return. However, if you plan on rebalancing much more frequently, there is a case to be made for lowering the span in order to capture recent trends.

`pypfopt.expected_returns.``capm_return`(_prices_, _market\_prices=None_, _returns\_data=False_, _risk\_free\_rate=0.02_, _compounding=True_, _frequency=252_, _log\_returns=False_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/latest/_modules/pypfopt/expected_returns.html#capm_return)

[¶](https://pyportfolioopt.readthedocs.io/en/latest/ExpectedReturns.html#pypfopt.expected_returns.capm_return "Permalink to this definition")

Compute a return estimate using the Capital Asset Pricing Model. Under the CAPM, asset returns are equal to market returns plus a \\(�eta\\) term encoding the relative risk of the asset.

\\\[R\_i = R\_f + \\beta\_i (E(R\_m) - R\_f)\\\]

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **market\_prices** (_pd.DataFrame__,_ _optional_) – adjusted closing prices of the benchmark, defaults to None

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first arguments are returns instead of prices.

* **risk\_free\_rate** (_float__,_ _optional_) – risk-free rate of borrowing/lending, defaults to 0.02. You should use the appropriate time period, corresponding to the frequency parameter.

* **compounding** (_bool__,_ _defaults to True_) – computes geometric mean returns if True, arithmetic otherwise, optional.

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year)

* **log\_returns** (_bool__,_ _defaults to False_) – whether to compute using log returns |

| Returns: | annualised return estimate |

| Return type: | pd.Series |

`pypfopt.expected_returns.``returns_from_prices`(_prices_, _log\_returns=False_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/latest/_modules/pypfopt/expected_returns.html#returns_from_prices)

[¶](https://pyportfolioopt.readthedocs.io/en/latest/ExpectedReturns.html#pypfopt.expected_returns.returns_from_prices "Permalink to this definition")

Calculate the returns given prices.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted (daily) closing prices of the asset, each row is a date and each column is a ticker/id.

* **log\_returns** (_bool__,_ _defaults to False_) – whether to compute using log returns |

| Returns: | (daily) returns |

| Return type: | pd.DataFrame |

`pypfopt.expected_returns.``prices_from_returns`(_returns_, _log\_returns=False_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/latest/_modules/pypfopt/expected_returns.html#prices_from_returns)

[¶](https://pyportfolioopt.readthedocs.io/en/latest/ExpectedReturns.html#pypfopt.expected_returns.prices_from_returns "Permalink to this definition")

Calculate the pseudo-prices given returns. These are not true prices because the initial prices are all set to 1, but it behaves as intended when passed to any PyPortfolioOpt method.

| | |

| --- | --- |

| Parameters: | * **returns** (_pd.DataFrame_) – (daily) percentage returns of the assets

* **log\_returns** (_bool__,_ _defaults to False_) – whether to compute using log returns |

| Returns: | (daily) pseudo-prices. |

| Return type: | pd.DataFrame |

---

# Risk Models — PyPortfolioOpt 1.4.1 documentation

* [Docs](https://pyportfolioopt.readthedocs.io/en/stable/index.html)

»

* Risk Models

* [Edit on GitHub](https://github.com/robertmartin8/PyPortfolioOpt/blob/1db089602dee348f1eade9b981ca21cd35f1dcca/docs/RiskModels.rst)

* * *

Risk Models[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#risk-models "Permalink to this headline")

=========================================================================================================================

In addition to the expected returns, mean-variance optimization requires a **risk model**, some way of quantifying asset risk. The most commonly-used risk model is the covariance matrix, which describes asset volatilities and their co-dependence. This is important because one of the principles of diversification is that risk can be reduced by making many uncorrelated bets (correlation is just normalised covariance).

[](https://pyportfolioopt.readthedocs.io/en/stable/_images/corrplot.png)

In many ways, the subject of risk models is far more important than that of expected returns because historical variance is generally a much more persistent statistic than mean historical returns. In fact, research by Kritzman et al. (2010) [\[1\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id9)

suggests that minimum variance portfolios, formed by optimising without providing expected returns, actually perform much better out of sample.

The problem, however, is that in practice we do not have access to the covariance matrix (in the same way that we don’t have access to expected returns) – the only thing we can do is to make estimates based on past data. The most straightforward approach is to just calculate the **sample covariance matrix** based on historical returns, but relatively recent (post-2000) research indicates that there are much more robust statistical estimators of the covariance matrix. In addition to providing a wrapper around the estimators in `sklearn`, PyPortfolioOpt provides some experimental alternatives such as semicovariance and exponentially weighted covariance.

Attention

Estimation of the covariance matrix is a very deep and actively-researched topic that involves statistics, econometrics, and numerical/computational approaches. PyPortfolioOpt implements several options, but there is a lot of room for more sophistication.

The `risk_models` module provides functions for estimating the covariance matrix given historical returns.

The format of the data input is the same as that in [Expected Returns](https://pyportfolioopt.readthedocs.io/en/stable/ExpectedReturns.html#expected-returns)

.

**Currently implemented:**

* fix non-positive semidefinite matrices

* general risk matrix function, allowing you to run any risk model from one function.

* sample covariance

* semicovariance

* exponentially weighted covariance

* minimum covariance determinant

* shrunk covariance matrices:

> * manual shrinkage

> * Ledoit Wolf shrinkage

> * Oracle Approximating shrinkage

* covariance to correlation matrix

Note

For any of these methods, if you would prefer to pass returns (the default is prices), set the boolean flag `returns_data=True`

`pypfopt.risk_models.``risk_matrix`(_prices_, _method='sample\_cov'_, _\*\*kwargs_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#risk_matrix)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.risk_matrix "Permalink to this definition")

Compute a covariance matrix, using the risk model supplied in the `method` parameter.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices.

* **method** (_str__,_ _optional_) –

the risk model to use. Should be one of:

* `sample_cov`

* `semicovariance`

* `exp_cov`

* `ledoit_wolf`

* `ledoit_wolf_constant_variance`

* `ledoit_wolf_single_factor`

* `ledoit_wolf_constant_correlation`

* `oracle_approximating` |

| Raises: | **NotImplementedError** – if the supplied method is not recognised |

| Returns: | annualised sample covariance matrix |

| Return type: | pd.DataFrame |

`pypfopt.risk_models.``fix_nonpositive_semidefinite`(_matrix_, _fix\_method='spectral'_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#fix_nonpositive_semidefinite)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.fix_nonpositive_semidefinite "Permalink to this definition")

Check if a covariance matrix is positive semidefinite, and if not, fix it with the chosen method.

The `spectral` method sets negative eigenvalues to zero then rebuilds the matrix, while the `diag` method adds a small positive value to the diagonal.

| | |

| --- | --- |

| Parameters: | * **matrix** (_pd.DataFrame_) – raw covariance matrix (may not be PSD)

* **fix\_method** (_str__,_ _optional_) – {“spectral”, “diag”}, defaults to “spectral” |

| Raises: | **NotImplementedError** – if a method is passed that isn’t implemented |

| Returns: | positive semidefinite covariance matrix |

| Return type: | pd.DataFrame |

Not all the calculated covariance matrices will be positive semidefinite (PSD). This method checks if a matrix is PSD and fixes it if not.

`pypfopt.risk_models.``sample_cov`(_prices_, _returns\_data=False_, _frequency=252_, _\*\*kwargs_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#sample_cov)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.sample_cov "Permalink to this definition")

Calculate the annualised sample covariance matrix of (daily) asset returns.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices.

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year) |

| Returns: | annualised sample covariance matrix |

| Return type: | pd.DataFrame |

This is the textbook default approach. The entries in the sample covariance matrix (which we denote as _S_) are the sample covariances between the _i_ th and _j_ th asset (the diagonals consist of variances). Although the sample covariance matrix is an unbiased estimator of the covariance matrix, i.e \\(E(S) = \\Sigma\\), in practice it suffers from misspecification error and a lack of robustness. This is particularly problematic in mean-variance optimization, because the optimizer may give extra credence to the erroneous values.

Note

This should _not_ be your default choice! Please use a shrinkage estimator instead.

`pypfopt.risk_models.``semicovariance`(_prices_, _returns\_data=False_, _benchmark=7.9e-05_, _frequency=252_, _\*\*kwargs_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#semicovariance)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.semicovariance "Permalink to this definition")

Estimate the semicovariance matrix, i.e the covariance given that the returns are less than the benchmark.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices.

* **benchmark** (_float_) – the benchmark return, defaults to the daily risk-free rate, i.e \\(1.02^{(1/252)} -1\\).

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year). Ensure that you use the appropriate benchmark, e.g if `frequency=12` use the monthly risk-free rate. |

| Returns: | semicovariance matrix |

| Return type: | pd.DataFrame |

The semivariance is the variance of all returns which are below some benchmark _B_ (typically the risk-free rate) – it is a common measure of downside risk. There are multiple possible ways of defining a semicovariance matrix, the main differences lying in the ‘pairwise’ nature, i.e whether we should sum over \\(\\min(r\_i,B)\\min(r\_j,B)\\) or \\(\\min(r\_ir\_j, B)\\). In this implementation, we have followed the advice of Estrada (2007) [\[2\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id10)

, preferring:

\\\[\\frac{1}{n}\\sum\_{i = 1}^n {\\sum\_{j = 1}^n {\\min \\left( {{r\_i},B} \\right)} } \\min \\left( {{r\_j},B} \\right)\\\]

`pypfopt.risk_models.``exp_cov`(_prices_, _returns\_data=False_, _span=180_, _frequency=252_, _\*\*kwargs_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#exp_cov)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.exp_cov "Permalink to this definition")

Estimate the exponentially-weighted covariance matrix, which gives greater weight to more recent data.

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices.

* **span** (_int__,_ _optional_) – the span of the exponential weighting function, defaults to 180

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year) |

| Returns: | annualised estimate of exponential covariance matrix |

| Return type: | pd.DataFrame |

The exponential covariance matrix is a novel way of giving more weight to recent data when calculating covariance, in the same way that the exponential moving average price is often preferred to the simple average price. For a full explanation of how this estimator works, please refer to the [blog post](https://reasonabledeviations.com/2018/08/15/exponential-covariance/)

on my academic website.

`pypfopt.risk_models.``cov_to_corr`(_cov\_matrix_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#cov_to_corr)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.cov_to_corr "Permalink to this definition")

Convert a covariance matrix to a correlation matrix.

| | |

| --- | --- |

| Parameters: | **cov\_matrix** (_pd.DataFrame_) – covariance matrix |

| Returns: | correlation matrix |

| Return type: | pd.DataFrame |

`pypfopt.risk_models.``corr_to_cov`(_corr\_matrix_, _stdevs_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#corr_to_cov)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.corr_to_cov "Permalink to this definition")

Convert a correlation matrix to a covariance matrix

| | |

| --- | --- |

| Parameters: | * **corr\_matrix** (_pd.DataFrame_) – correlation matrix

* **stdevs** (_array-like_) – vector of standard deviations |

| Returns: | covariance matrix |

| Return type: | pd.DataFrame |

Shrinkage estimators[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#shrinkage-estimators "Permalink to this headline")

-------------------------------------------------------------------------------------------------------------------------------------------

A great starting point for those interested in understanding shrinkage estimators is _Honey, I Shrunk the Sample Covariance Matrix_ [\[3\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id11)

by Ledoit and Wolf, which does a good job at capturing the intuition behind them – we will adopt the notation used therein. I have written a summary of this article, which is available on my [website](https://reasonabledeviations.com/notes/papers/ledoit_wolf_covariance/)

. A more rigorous reference can be found in Ledoit and Wolf (2001) [\[4\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id12)

.

The essential idea is that the unbiased but often poorly estimated sample covariance can be combined with a structured estimator \\(F\\), using the below formula (where \\(\\delta\\) is the shrinkage constant):

\\\[\\hat{\\Sigma} = \\delta F + (1-\\delta) S\\\]

It is called shrinkage because it can be thought of as “shrinking” the sample covariance matrix towards the other estimator, which is accordingly called the **shrinkage target**. The shrinkage target may be significantly biased but has little estimation error. There are many possible options for the target, and each one will result in a different optimal shrinkage constant \\(\\delta\\). PyPortfolioOpt offers the following shrinkage methods:

* Ledoit-Wolf shrinkage:

> * `constant_variance` shrinkage, i.e the target is the diagonal matrix with the mean of asset variances on the diagonals and zeroes elsewhere. This is the shrinkage offered by `sklearn.LedoitWolf`.

> * `single_factor` shrinkage. Based on Sharpe’s single-index model which effectively uses a stock’s beta to the market as a risk model. See Ledoit and Wolf 2001 [\[4\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id12)

> .

> * `constant_correlation` shrinkage, in which all pairwise correlations are set to the average correlation (sample variances are unchanged). See Ledoit and Wolf 2003 [\[3\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id11)

>

* Oracle approximating shrinkage (OAS), invented by Chen et al. (2010) [\[5\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id13)

, which has a lower mean-squared error than Ledoit-Wolf shrinkage when samples are Gaussian or near-Gaussian.

Tip

For most use cases, I would just go with Ledoit Wolf shrinkage, as recommended by [Quantopian](https://www.quantopian.com/)

in their lecture series on quantitative finance.

My implementations have been translated from the Matlab code on [Michael Wolf’s webpage](https://www.econ.uzh.ch/en/people/faculty/wolf/publications.html)

, with the help of [xtuanta](https://github.com/robertmartin8/PyPortfolioOpt/issues/20)

.

_class_ `pypfopt.risk_models.``CovarianceShrinkage`(_prices_, _returns\_data=False_, _frequency=252_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#CovarianceShrinkage)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.CovarianceShrinkage "Permalink to this definition")

Provide methods for computing shrinkage estimates of the covariance matrix, using the sample covariance matrix and choosing the structured estimator to be an identity matrix multiplied by the average sample variance. The shrinkage constant can be input manually, though there exist methods (notably Ledoit Wolf) to estimate the optimal value.

Instance variables:

* `X` - pd.DataFrame (returns)

* `S` - np.ndarray (sample covariance matrix)

* `delta` - float (shrinkage constant)

* `frequency` - int

`__init__`(_prices_, _returns\_data=False_, _frequency=252_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#CovarianceShrinkage.__init__)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.CovarianceShrinkage.__init__ "Permalink to this definition")

| | |

| --- | --- |

| Parameters: | * **prices** (_pd.DataFrame_) – adjusted closing prices of the asset, each row is a date and each column is a ticker/id.

* **returns\_data** (_bool__,_ _defaults to False._) – if true, the first argument is returns instead of prices.

* **frequency** (_int__,_ _optional_) – number of time periods in a year, defaults to 252 (the number of trading days in a year) |

`ledoit_wolf`(_shrinkage\_target='constant\_variance'_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#CovarianceShrinkage.ledoit_wolf)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.CovarianceShrinkage.ledoit_wolf "Permalink to this definition")

Calculate the Ledoit-Wolf shrinkage estimate for a particular shrinkage target.

| | |

| --- | --- |

| Parameters: | **shrinkage\_target** (_str__,_ _optional_) – choice of shrinkage target, either `constant_variance`, `single_factor` or `constant_correlation`. Defaults to `constant_variance`. |

| Raises: | **NotImplementedError** – if the shrinkage\_target is unrecognised |

| Returns: | shrunk sample covariance matrix |

| Return type: | np.ndarray |

`oracle_approximating`()[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#CovarianceShrinkage.oracle_approximating)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.CovarianceShrinkage.oracle_approximating "Permalink to this definition")

Calculate the Oracle Approximating Shrinkage estimate

| | |

| --- | --- |

| Returns: | shrunk sample covariance matrix |

| Return type: | np.ndarray |

`shrunk_covariance`(_delta=0.2_)[\[source\]](https://pyportfolioopt.readthedocs.io/en/stable/_modules/pypfopt/risk_models.html#CovarianceShrinkage.shrunk_covariance)

[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#pypfopt.risk_models.CovarianceShrinkage.shrunk_covariance "Permalink to this definition")

Shrink a sample covariance matrix to the identity matrix (scaled by the average sample variance). This method does not estimate an optimal shrinkage parameter, it requires manual input.

| | |

| --- | --- |

| Parameters: | **delta** (_float__,_ _optional_) – shrinkage parameter, defaults to 0.2. |

| Returns: | shrunk sample covariance matrix |

| Return type: | np.ndarray |

References[¶](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#references "Permalink to this headline")

-----------------------------------------------------------------------------------------------------------------------

| | |

| --- | --- |

| [\[1\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id2) | Kritzman, Page & Turkington (2010) [In defense of optimization: The fallacy of 1/N](https://www.cfapubs.org/doi/abs/10.2469/faj.v66.n2.6)

. Financial Analysts Journal, 66(2), 31-39. |

| | |

| --- | --- |

| [\[2\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id3) | Estrada (2006), [Mean-Semivariance Optimization: A Heuristic Approach](https://papers.ssrn.com/sol3/papers.cfm?abstract_id=1028206) |

| | |

| --- | --- |

| \[3\] | _([1](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id4)

, [2](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id7)

)_ Ledoit, O., & Wolf, M. (2003). [Honey, I Shrunk the Sample Covariance Matrix](http://www.ledoit.net/honey.pdf)

The Journal of Portfolio Management, 30(4), 110–119. [https://doi.org/10.3905/jpm.2004.110](https://doi.org/10.3905/jpm.2004.110) |

| | |

| --- | --- |

| \[4\] | _([1](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id5)

, [2](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id6)

)_ Ledoit, O., & Wolf, M. (2001). [Improved estimation of the covariance matrix of stock returns with an application to portfolio selection](http://www.ledoit.net/ole2.pdf)

, 10, 603–621. |

| | |

| --- | --- |

| [\[5\]](https://pyportfolioopt.readthedocs.io/en/stable/RiskModels.html#id8) | Chen et al. (2010), [Shrinkage Algorithms for MMSE Covariance Estimation](https://arxiv.org/pdf/0907.4698.pdf)

, IEEE Transactions on Signals Processing, 58(10), 5016-5029. |

---

# Installation — PyPortfolioOpt 1.4.1 documentation

* [Docs](https://pyportfolioopt.readthedocs.io/en/stable/#)

»

* Installation

* [Edit on GitHub](https://github.com/robertmartin8/PyPortfolioOpt/blob/1db089602dee348f1eade9b981ca21cd35f1dcca/docs/index.rst)

* * *

[](https://pyportfolioopt.readthedocs.io/en/stable/_images/logo_v1-grey.png)

[](https://www.python.org/)

[](https://pypi.org/project/PyPortfolioOpt/)

[](https://opensource.org/licenses/MIT)

[](https://github.com/robertmartin8/PyPortfolioOpt/graphs/commit-activity)

PyPortfolioOpt is a library that implements portfolio optimization methods, including classical efficient frontier techniques and Black-Litterman allocation, as well as more recent developments in the field like shrinkage and Hierarchical Risk Parity, along with some novel experimental features like exponentially-weighted covariance matrices.

It is **extensive** yet easily **extensible**, and can be useful for both the casual investor and the serious practitioner. Whether you are a fundamentals-oriented investor who has identified a handful of undervalued picks, or an algorithmic trader who has a basket of strategies, PyPortfolioOpt can help you combine your alpha sources in a risk-efficient way.

Installation[¶](https://pyportfolioopt.readthedocs.io/en/stable/#installation "Permalink to this headline")

============================================================================================================

If you would like to play with PyPortfolioOpt interactively in your browser, you may launch Binder [here](https://mybinder.org/v2/gh/robertmartin8/pyportfolioopt/master/?filepath=cookbook)

. It takes a while to set up, but it lets you try out the cookbook recipes without having to install anything.

Prior to installing PyPortfolioOpt, you need to install C++. On macOS, this means that you need to install XCode Command Line Tools (see [here](https://osxdaily.com/2014/02/12/install-command-line-tools-mac-os-x/)

).

For Windows users, download Visual Studio [here](https://visualstudio.microsoft.com/thank-you-downloading-visual-studio/?sku=BuildTools&rel=16)

, with additional instructions [here](https://drive.google.com/file/d/0B4GsMXCRaSSIOWpYQkstajlYZ0tPVkNQSElmTWh1dXFaYkJr/view)

.

Installation can then be done via pip:

pip install PyPortfolioOpt

For the sake of best practice, it is good to do this with a dependency manager. I suggest you set yourself up with [poetry](https://github.com/sdispater/poetry)

, then within a new poetry project run:

poetry add PyPortfolioOpt

The alternative is to clone/download the project, then in the project directory run

python setup.py install

Thanks to Thomas Schmelzer, PyPortfolioOpt now supports Docker (requires **make**, **docker**, **docker-compose**). Build your first container with `make build`; run tests with `make test`. For more information, please read [this guide](https://docker-curriculum.com/#introduction)

.

Note

If any of these methods don’t work, please [raise an issue](https://github.com/robertmartin8/PyPortfolioOpt/issues)

with the ‘packaging’ label on GitHub

For developers[¶](https://pyportfolioopt.readthedocs.io/en/stable/#for-developers "Permalink to this headline")

----------------------------------------------------------------------------------------------------------------

If you are planning on using PyPortfolioOpt as a starting template for significant modifications, it probably makes sense to clone the repository and to just use the source code

git clone https://github.com/robertmartin8/PyPortfolioOpt

Alternatively, if you still want the convenience of a global `from pypfopt import x`, you should try

pip install -e git+https://github.com/robertmartin8/PyPortfolioOpt.git

A Quick Example[¶](https://pyportfolioopt.readthedocs.io/en/stable/#a-quick-example "Permalink to this headline")

==================================================================================================================

This section contains a quick look at what PyPortfolioOpt can do. For a guided tour, please check out the [User Guide](https://pyportfolioopt.readthedocs.io/en/stable/UserGuide.html#user-guide)

. For even more examples, check out the Jupyter notebooks in the [cookbook](https://github.com/robertmartin8/PyPortfolioOpt/tree/master/cookbook)

.

If you already have expected returns `mu` and a risk model `S` for your set of assets, generating an optimal portfolio is as easy as:

from pypfopt.efficient\_frontier import EfficientFrontier

ef \= EfficientFrontier(mu, S)

weights \= ef.max\_sharpe()