# Table of Contents

- [Riskfolio-Lib 7.2](#riskfolio-lib-7-2)

- [Advanced Portfolio Optimization: A Cutting-edge Quantitative Approach - Riskfolio-Lib 7.2](#advanced-portfolio-optimization-a-cutting-edge-quantitative-approach-riskfolio-lib-7-2)

- [Install - Riskfolio-Lib 7.2](#install-riskfolio-lib-7-2)

- [Examples - Riskfolio-Lib 7.2](#examples-riskfolio-lib-7-2)

- [Authors - Riskfolio-Lib 7.2](#authors-riskfolio-lib-7-2)

- [Contributing - Riskfolio-Lib 7.2](#contributing-riskfolio-lib-7-2)

- [License - Riskfolio-Lib 7.2](#license-riskfolio-lib-7-2)

- [Changelog - Riskfolio-Lib 7.2](#changelog-riskfolio-lib-7-2)

- [Reports Functions - Riskfolio-Lib 7.2](#reports-functions-riskfolio-lib-7-2)

- [Python Module Index - Riskfolio-Lib 7.2](#python-module-index-riskfolio-lib-7-2)

- [Index - Riskfolio-Lib 7.2](#index-riskfolio-lib-7-2)

- [Riskfolio-XL: Riskfolio-Lib add-in for Microsoft Excel - Riskfolio-Lib 7.2](#riskfolio-xl-riskfolio-lib-add-in-for-microsoft-excel-riskfolio-lib-7-2)

- [Portfolio Optimization with Python Course - Riskfolio-Lib 7.2](#portfolio-optimization-with-python-course-riskfolio-lib-7-2)

- [Hierarchical Clustering Portfolio Optimization - Riskfolio-Lib 7.2](#hierarchical-clustering-portfolio-optimization-riskfolio-lib-7-2)

- [Portfolio Optimization - Riskfolio-Lib 7.2](#portfolio-optimization-riskfolio-lib-7-2)

- [Parameters Estimation - Riskfolio-Lib 7.2](#parameters-estimation-riskfolio-lib-7-2)

- [Constraints Functions - Riskfolio-Lib 7.2](#constraints-functions-riskfolio-lib-7-2)

- [Plot Functions - Riskfolio-Lib 7.2](#plot-functions-riskfolio-lib-7-2)

- [Risk Functions - Riskfolio-Lib 7.2](#risk-functions-riskfolio-lib-7-2)

- [DBHT, OWA Weights, Gerber Statistic, CPP and Auxiliary Functions - Riskfolio-Lib 7.2](#dbht-owa-weights-gerber-statistic-cpp-and-auxiliary-functions-riskfolio-lib-7-2)

- [

Documentation page not found

- Read the Docs Community ](#-documentation-page-not-found-read-the-docs-community-)

- [Riskfolio-Lib 7.2](#riskfolio-lib-7-2)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

- [Just a moment...](#just-a-moment-)

---

# Riskfolio-Lib 7.2

[Skip to content](https://riskfolio-lib.readthedocs.io/en/latest/#portfolio-optimization-in-python-easy-for-everyone)

Riskfolio-Lib[¶](https://riskfolio-lib.readthedocs.io/en/latest/#riskfolio-lib "Link to this heading")

=======================================================================================================

Portfolio Optimization in Python, Easy for Everyone[¶](https://riskfolio-lib.readthedocs.io/en/latest/#portfolio-optimization-in-python-easy-for-everyone "Link to this heading")

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

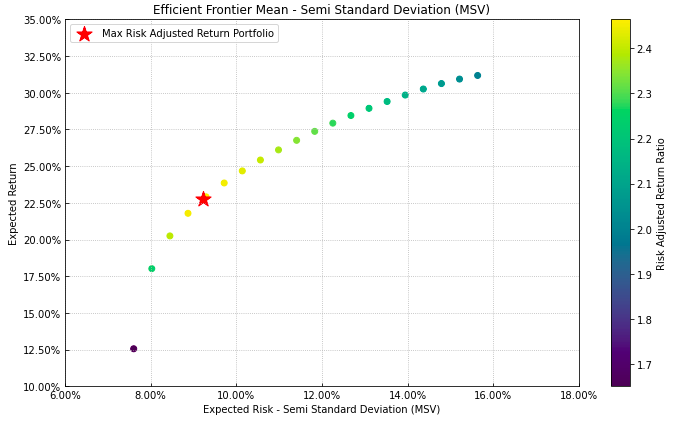

[](https://riskfolio-lib.readthedocs.io/en/latest/_images/MSV_Frontier.png)

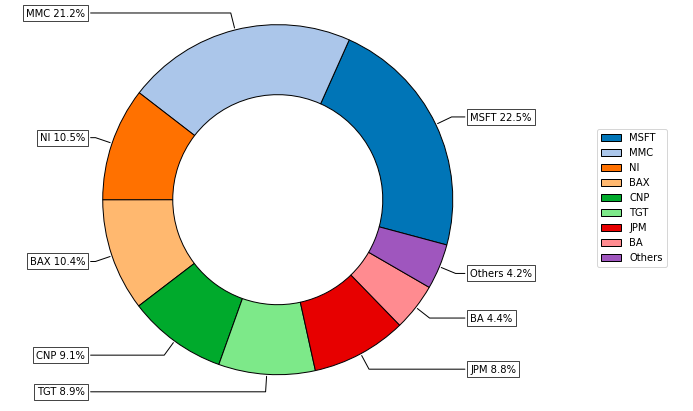

[](https://riskfolio-lib.readthedocs.io/en/latest/_images/Pie_Chart.png)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

[](https://github.com/dcajasn/Riskfolio-Lib/stargazers)

[](https://pepy.tech/project/riskfolio-lib)

[](https://pepy.tech/project/riskfolio-lib)

[](https://github.com/dcajasn/Riskfolio-Lib/blob/master/LICENSE.txt)

[](https://mybinder.org/v2/gh/dcajasn/Riskfolio-Lib/HEAD)

### Description[¶](https://riskfolio-lib.readthedocs.io/en/latest/#description "Link to this heading")

Riskfolio-Lib is a library for making **Portfolio Optimization in Python** made in Peru 🇵🇪. Its objective is to help students, academics and practitioners to build investment portfolios based on mathematically complex models with low effort. It is built on top of [CVXPY](https://www.cvxpy.org/)

and closely integrated with [Pandas](https://pandas.pydata.org/)

data structures.

Some of key functionalities that Riskfolio-Lib offers:

* Mean Risk and Logarithmic Mean Risk (Kelly Criterion) Portfolio Optimization with 4 objective functions:

> * Minimum Risk.

>

> * Maximum Return.

>

> * Maximum Utility Function.

>

> * Maximum Risk Adjusted Return Ratio.

>

* Mean Risk and Logarithmic Mean Risk (Kelly Criterion) Portfolio Optimization with 24 convex risk measures:

> **Dispersion Risk Measures:**

>

> * Standard Deviation.

>

> * Square Root Kurtosis.

>

> * Mean Absolute Deviation (MAD).

>

> * Gini Mean Difference (GMD).

>

> * Conditional Value at Risk Range.

>

> * Tail Gini Range.

>

> * Entropic Value at Risk Range.

>

> * Relativistic Value at Risk Range.

>

> * Range.

>

>

> **Downside Risk Measures:**

>

> * Semi Standard Deviation.

>

> * Square Root Semi Kurtosis.

>

> * First Lower Partial Moment (Omega Ratio).

>

> * Second Lower Partial Moment (Sortino Ratio).

>

> * Conditional Value at Risk (CVaR).

>

> * Tail Gini.

>

> * Entropic Value at Risk (EVaR).

>

> * Relativistic Value at Risk (RLVaR).

>

> * Worst Realization (Minimax).

>

>

> **Drawdown Risk Measures:**

>

> * Average Drawdown for uncompounded cumulative returns.

>

> * Ulcer Index for uncompounded cumulative returns.

>

> * Conditional Drawdown at Risk (CDaR) for uncompounded cumulative returns.

>

> * Entropic Drawdown at Risk (EDaR) for uncompounded cumulative returns.

>

> * Relativistic Drawdown at Risk (RLDaR) for uncompounded cumulative returns.

>

> * Maximum Drawdown (Calmar Ratio) for uncompounded cumulative returns.

>

* Risk Parity Portfolio Optimization with 20 convex risk measures:

> **Dispersion Risk Measures:**

>

> * Standard Deviation.

>

> * Square Root Kurtosis.

>

> * Mean Absolute Deviation (MAD).

>

> * Gini Mean Difference (GMD).

>

> * Conditional Value at Risk Range.

>

> * Tail Gini Range.

>

> * Entropic Value at Risk Range.

>

> * Relativistic Value at Risk Range.

>

>

> **Downside Risk Measures:**

>

> * Semi Standard Deviation.

>

> * Square Root Semi Kurtosis.

>

> * First Lower Partial Moment (Omega Ratio)

>

> * Second Lower Partial Moment (Sortino Ratio)

>

> * Conditional Value at Risk (CVaR).

>

> * Tail Gini.

>

> * Entropic Value at Risk (EVaR).

>

> * Relativistic Value at Risk (RLVaR).

>

>

> **Drawdown Risk Measures:**

>

> * Ulcer Index for uncompounded cumulative returns.

>

> * Conditional Drawdown at Risk (CDaR) for uncompounded cumulative returns.

>

> * Entropic Drawdown at Risk (EDaR) for uncompounded cumulative returns.

>

> * Relativistic Drawdown at Risk (RLDaR) for uncompounded cumulative returns.

>

* Hierarchical Clustering Portfolio Optimization: Hierarchical Risk Parity (HRP) and Hierarchical Equal Risk Contribution (HERC) with 35 risk measures using naive risk parity:

> **Dispersion Risk Measures:**

>

> * Standard Deviation.

>

> * Variance.

>

> * Square Root Kurtosis.

>

> * Mean Absolute Deviation (MAD).

>

> * Gini Mean Difference (GMD).

>

> * Value at Risk Range.

>

> * Conditional Value at Risk Range.

>

> * Tail Gini Range.

>

> * Entropic Value at Risk Range.

>

> * Relativistic Value at Risk Range.

>

> * Range.

>

>

> **Downside Risk Measures:**

>

> * Semi Standard Deviation.

>

> * Square Root Semi Kurtosis.

>

> * First Lower Partial Moment (Omega Ratio).

>

> * Second Lower Partial Moment (Sortino Ratio).

>

> * Value at Risk (VaR).

>

> * Conditional Value at Risk (CVaR).

>

> * Entropic Value at Risk (EVaR).

>

> * Relativistic Value at Risk (RLVaR).

>

> * Tail Gini.

>

> * Worst Case Realization (Minimax).

>

>

> **Drawdown Risk Measures:**

>

> * Average Drawdown for compounded and uncompounded cumulative returns.

>

> * Ulcer Index for compounded and uncompounded cumulative returns.

>

> * Drawdown at Risk (DaR) for compounded and uncompounded cumulative returns.

>

> * Conditional Drawdown at Risk (CDaR) for compounded and uncompounded cumulative returns.

>

> * Entropic Drawdown at Risk (EDaR) for compounded and uncompounded cumulative returns.

>

> * Relativistic Drawdown at Risk (RLDaR) for compounded and uncompounded cumulative returns.

>

> * Maximum Drawdown (Calmar Ratio) for compounded and uncompounded cumulative returns.

>

* Nested Clustered Optimization (NCO) with four objective functions and the available risk measures to each objective:

> * Minimum Risk.

>

> * Maximum Return.

>

> * Maximum Utility Function.

>

> * Equal Risk Contribution.

>

* Worst Case Mean Variance Portfolio Optimization.

* Relaxed Risk Parity Portfolio Optimization.

* Ordered Weighted Averaging (OWA) Portfolio Optimization.

* Portfolio optimization with Black Litterman model.

* Portfolio optimization with Risk Factors model.

* Portfolio optimization with Black Litterman Bayesian model.

* Portfolio optimization with Augmented Black Litterman model.

* Portfolio optimization with constraints on tracking error and turnover.

* Portfolio optimization with short positions and leveraged portfolios.

* Portfolio optimization with constraints on number of assets and number of effective assets.

* Portfolio optimization with constraints based on graph information.

* Portfolio optimization with inequality constraints on risk contributions for variance.

* Portfolio optimization with inequality constraints on factor risk contributions for variance.

* Portfolio optimization with integer constraints such as Cardinality on Assets and Categories, Mutually Exclusive and Join Investment.

* Tools to build efficient frontier for 24 convex risk measures.

* Tools to build linear constraints on assets, asset classes and risk factors.

* Tools to build views on assets and asset classes.

* Tools to build views on risk factors.

* Tools to build risk contribution constraints per asset classes.

* Tools to build risk contribution constraints per risk factor using explicit risk factors and principal components.

* Tools to build bounds constraints for Hierarchical Clustering Portfolios.

* Tools to calculate risk measures.

* Tools to calculate risk contributions per asset.

* Tools to calculate risk contributions per risk factor.

* Tools to calculate uncertainty sets for mean vector and covariance matrix.

* Tools to calculate assets clusters based on codependence metrics.

* Tools to estimate loadings matrix (Stepwise Regression and Principal Components Regression).

* Tools to visualizing portfolio properties and risk measures.

* Tools to build reports on Jupyter Notebook and Excel.

* Option to use commercial optimization solver like MOSEK or GUROBI for large scale problems.

### Choosing a Solver[¶](https://riskfolio-lib.readthedocs.io/en/latest/#choosing-a-solver "Link to this heading")

Due to Riskfolio-Lib is based on CVXPY, Riskfolio-Lib can use the same solvers available for CVXPY. The list of solvers compatible with CVXPY is available in [Choosing a solver](https://www.cvxpy.org/tutorial/solvers/index.html#choosing-a-solver)

section of CVXPY’s documentation. However, to select an adequate solver for each risk measure we can use the following table that specifies which type of programming technique is used to model each risk measure.

| Risk Measure | LP | QP | SOCP | SDP | EXP | POW |

| --- | --- | --- | --- | --- | --- | --- |

| Variance (MV) | | | X | X\* | | |

| Mean Absolute Deviation (MAD) | X | | | | | |

| Gini Mean Difference (GMD) | | | | | | X\*\* |

| Semi Variance (MSV) | | | X | | | |

| Kurtosis (KT) | | | | X | | |

| Semi Kurtosis (SKT) | | | | X | | |

| First Lower Partial Moment (FLPM) | X | | | | | |

| Second Lower Partial Moment (SLPM) | | | X | | | |

| Conditional Value at Risk (CVaR) | X | | | | | |

| Tail Gini (TG) | | | | | | X\*\* |

| Entropic Value at Risk (EVaR) | | | | | X\*\* | |

| Relativistic Value at Risk (RLVaR) | | | | | | X\*\* |

| Worst Realization (WR) | X | | | | | |

| CVaR Range (CVRG) | X | | | | | |

| Tail Gini Range (TGRG) | | | | | | X\*\* |

| EVaR Range (EVRG) | | | | | X\*\* | |

| RLVaR Range (RVRG) | | | | | | X\*\* |

| Range (RG) | X | | | | | |

| Average Drawdown (ADD) | X | | | | | |

| Ulcer Index (UCI) | | | X | | | |

| Conditional Drawdown at Risk (CDaR) | X | | | | | |

| Entropic Drawdown at Risk (EDaR) | | | | | X\*\* | |

| Relativistic Drawdown at Risk (RLDaR) | | | | | | X\*\* |

| Maximum Drawdown (MDD) | X | | | | | |

(\*) When SDP graph theory constraints or risk contribution constraints are included. In the case integer programming graph theory constraints are included, the model assume the SOCP formulation.

(\*\*) For these models is highly recommended to use MOSEK as solver, due to in some cases CLARABEL cannot find a solution and SCS takes too much time to solve them.

LP: Linear Programming refers to problems with a linear objective function and linear constraints.

QP: Quadratic Programming refers to problems with a quadratic objective function and linear constraints.

SOCP: Second Order Cone Programming refers to problems with second-order cone constraints.

SDP: Semidefinite Programming refers to problems with positive semidefinite constraints.

EXP:refers to problems with exponential cone constraints.

POW: refers to problems with 3-dimensional power cone constraints.

### Consulting Fees[¶](https://riskfolio-lib.readthedocs.io/en/latest/#consulting-fees "Link to this heading")

Riskfolio-Lib is an open-source project, however due it’s a project that is not financed for any institution, I started charging for consultancies that are not related to errors in source code. Our fees are as follows:

* $ 25 USD (United States Dollars) per question that doesn’t require to check code.

* $ 50 USD to check a small size script or code (less than 200 lines of code). The fee of the solution depends on the complexity of the solution:

* $ 50 USD for simple errors in scripts (modify less than 10 lines of code).

* For most complex errors the fee depends on the complexity of the solution but the fee is $ 150 USD per hour.

* $ 100 USD to check a medium size script or code (between 201 and 600 lines of code). The fee of the solution depends on the complexity of the solution:

* $ 50 USD for simple errors in scripts (modify less than 10 lines of code).

* For most complex errors the fee depends on the complexity of the solution but the fee is $ 150 USD per hour.

* For large size script or code (more than 600 lines of code) the fee is variable depending on the size of the code. The fee of the solution depends on the complexity of the solution:

* $ 50 USD for simple errors in scripts (modify less than 10 lines of code).

* For most complex errors the fee depends on the complexity of the solution but the fee is $ 150 USD per hour.

**All consulting must be paid in advance**.

You can contact me through:

* LinkedIn

* Gmail

You can pay using one of the following channels:

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

### Citing[¶](https://riskfolio-lib.readthedocs.io/en/latest/#citing "Link to this heading")

If you use Riskfolio-Lib for published work, please use the following BibTeX entry:

`@misc{riskfolio, author = {Dany Cajas}, title = {Riskfolio-Lib (7.2.1)}, year = {2026}, url = {https://github.com/dcajasn/Riskfolio-Lib}, }`

### Contents[¶](https://riskfolio-lib.readthedocs.io/en/latest/#contents "Link to this heading")

* [Portfolio Optimization Book](https://riskfolio-lib.readthedocs.io/en/latest/book.html)

* [Portfolio Optimization Course](https://riskfolio-lib.readthedocs.io/en/latest/course.html)

* [Riskfolio-XL](https://riskfolio-lib.readthedocs.io/en/latest/excel.html)

* [Install](https://riskfolio-lib.readthedocs.io/en/latest/install.html)

* [Portfolio Models](https://riskfolio-lib.readthedocs.io/en/latest/portfolio.html)

* [Hierarchical Clustering Models](https://riskfolio-lib.readthedocs.io/en/latest/hcportfolio.html)

* [Parameters Estimation](https://riskfolio-lib.readthedocs.io/en/latest/parameters.html)

* [Constraints Functions](https://riskfolio-lib.readthedocs.io/en/latest/constraints.html)

* [Risk Functions](https://riskfolio-lib.readthedocs.io/en/latest/risk.html)

* [Plot Functions](https://riskfolio-lib.readthedocs.io/en/latest/plot.html)

* [Reports](https://riskfolio-lib.readthedocs.io/en/latest/reports.html)

* [Auxiliary Functions](https://riskfolio-lib.readthedocs.io/en/latest/auxiliary.html)

* [Examples](https://riskfolio-lib.readthedocs.io/en/latest/examples.html)

* [Contributing](https://riskfolio-lib.readthedocs.io/en/latest/contributing.html)

* [Authors](https://riskfolio-lib.readthedocs.io/en/latest/authors.html)

* [License](https://riskfolio-lib.readthedocs.io/en/latest/license.html)

* [Changelog](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html)

### Indices and tables[¶](https://riskfolio-lib.readthedocs.io/en/latest/#indices-and-tables "Link to this heading")

* [Index](https://riskfolio-lib.readthedocs.io/en/latest/genindex.html)

* [Module Index](https://riskfolio-lib.readthedocs.io/en/latest/py-modindex.html)

* [Search Page](https://riskfolio-lib.readthedocs.io/en/latest/search.html)

### Module Plans[¶](https://riskfolio-lib.readthedocs.io/en/latest/#module-plans "Link to this heading")

The plan for this library is to add more functions that will be very useful for students, academics and practitioners.

* Add more functions based on suggestion of users.

[**On-Demand H100 SXM GPUs for $2.99/hr/GPU with Lambda** 640 GB of vRAM in one 8x instance **Launch now**](https://server.ethicalads.io/proxy/click/9837/019d0edd-8fac-7681-b3ae-6e1cc74dab4a/)

[Ads by EthicalAds](https://www.ethicalads.io/advertisers/topics/data-science/?ref=ea-text)

---

# Advanced Portfolio Optimization: A Cutting-edge Quantitative Approach - Riskfolio-Lib 7.2

[Skip to content](https://riskfolio-lib.readthedocs.io/en/latest/book.html#motivation)

Advanced Portfolio Optimization: A Cutting-edge Quantitative Approach[¶](https://riskfolio-lib.readthedocs.io/en/latest/book.html#advanced-portfolio-optimization-a-cutting-edge-quantitative-approach "Link to this heading")

===============================================================================================================================================================================================================================

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

Motivation[¶](https://riskfolio-lib.readthedocs.io/en/latest/book.html#motivation "Link to this heading")

----------------------------------------------------------------------------------------------------------

This book attempts to fill the gap that exists in quantitative finance books and courses that only focus on the mean-variance model and its variants, and ignore the further developments made in the last 70 years after the publication of Markowitz’s pioneering work. Readers will find this book very useful because each section explains the idea and mathematics of each model, and each section is accompanied by its corresponding Python code that allows all the examples to be reproduced.

Buy on Springer[¶](https://riskfolio-lib.readthedocs.io/en/latest/book.html#buy-on-springer "Link to this heading")

--------------------------------------------------------------------------------------------------------------------

Click the button below to buy on Springer Shop:

[Buy Advanced Portfolio Optimization Book on Springer](https://www.anrdoezrs.net/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

Table of Contents[¶](https://riskfolio-lib.readthedocs.io/en/latest/book.html#table-of-contents "Link to this heading")

------------------------------------------------------------------------------------------------------------------------

The detailed content of the book follows below:

---

# Install - Riskfolio-Lib 7.2

[Skip to content](https://riskfolio-lib.readthedocs.io/en/latest/install.html#mac-os-x-windows-and-linux)

Install[¶](https://riskfolio-lib.readthedocs.io/en/latest/install.html#install "Link to this heading")

=======================================================================================================

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

Mac OS X, Windows, and Linux[¶](https://riskfolio-lib.readthedocs.io/en/latest/install.html#mac-os-x-windows-and-linux "Link to this heading")

-----------------------------------------------------------------------------------------------------------------------------------------------

Riskfolio-lib only supports Python 3.7+ on OS X, Windows, and Linux. I recommend using pip for installation.

1. It is highly recommendable that you must have installed a scientific Python distribution like [anaconda](https://www.anaconda.com/products/individual)

or [winpython](https://winpython.github.io/)

(Windows only).

2. Install `Pybind11`.

> `pip install pybind11`

3. If you don’t have installed cvxpy, you must follow [cvxpy](https://www.cvxpy.org/install/index.html)

installation instructions before installing Riskfolio-Lib.

4. If you still have problems installing cvxpy, you can download cvxpy wheel from the [Unofficial Windows Binaries for Python Extension Packages](https://www.lfd.uci.edu/~gohlke/pythonlibs/#cvxpy)

and install using pip.

> `pip install path/cvxpy‑version.whl`

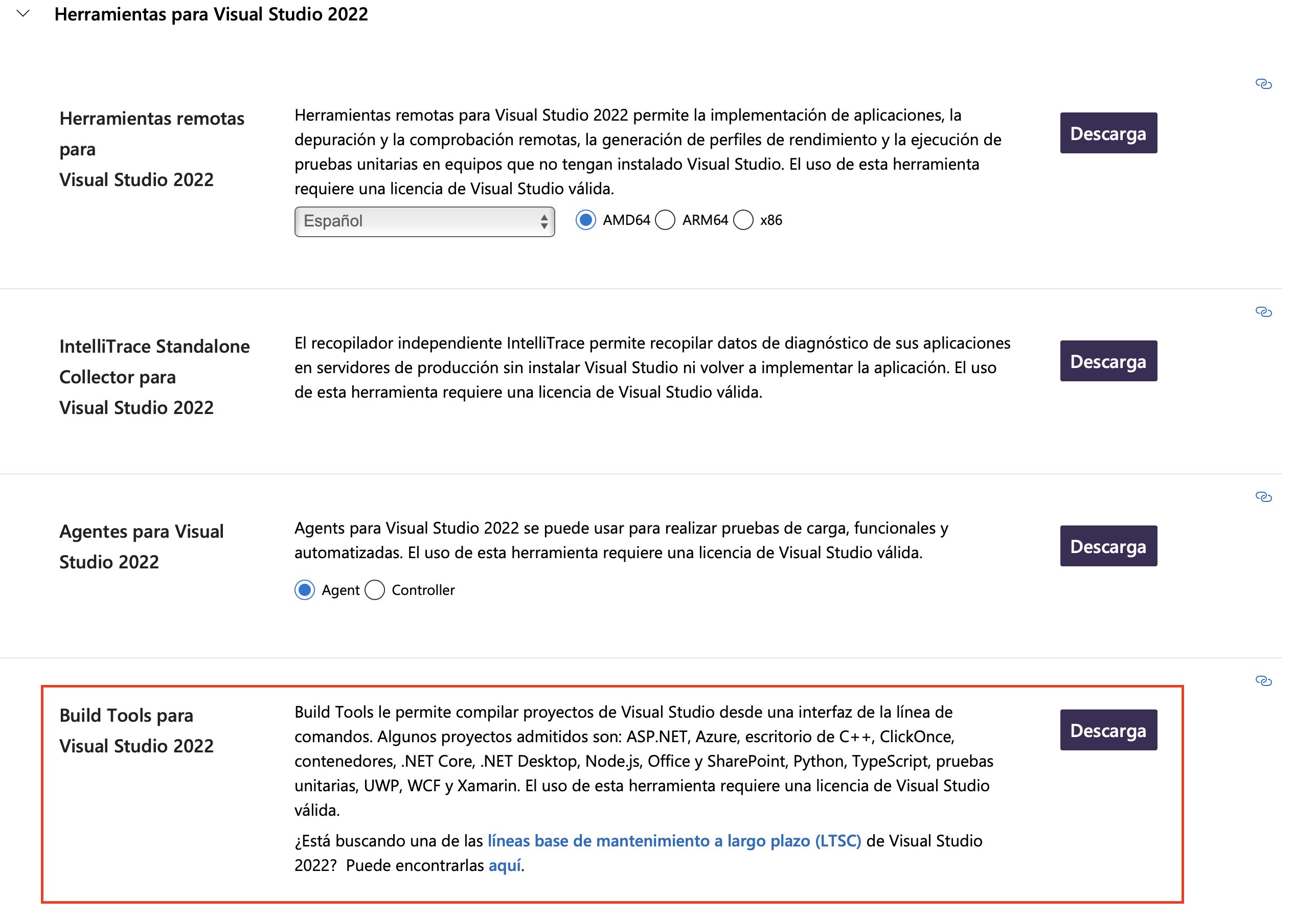

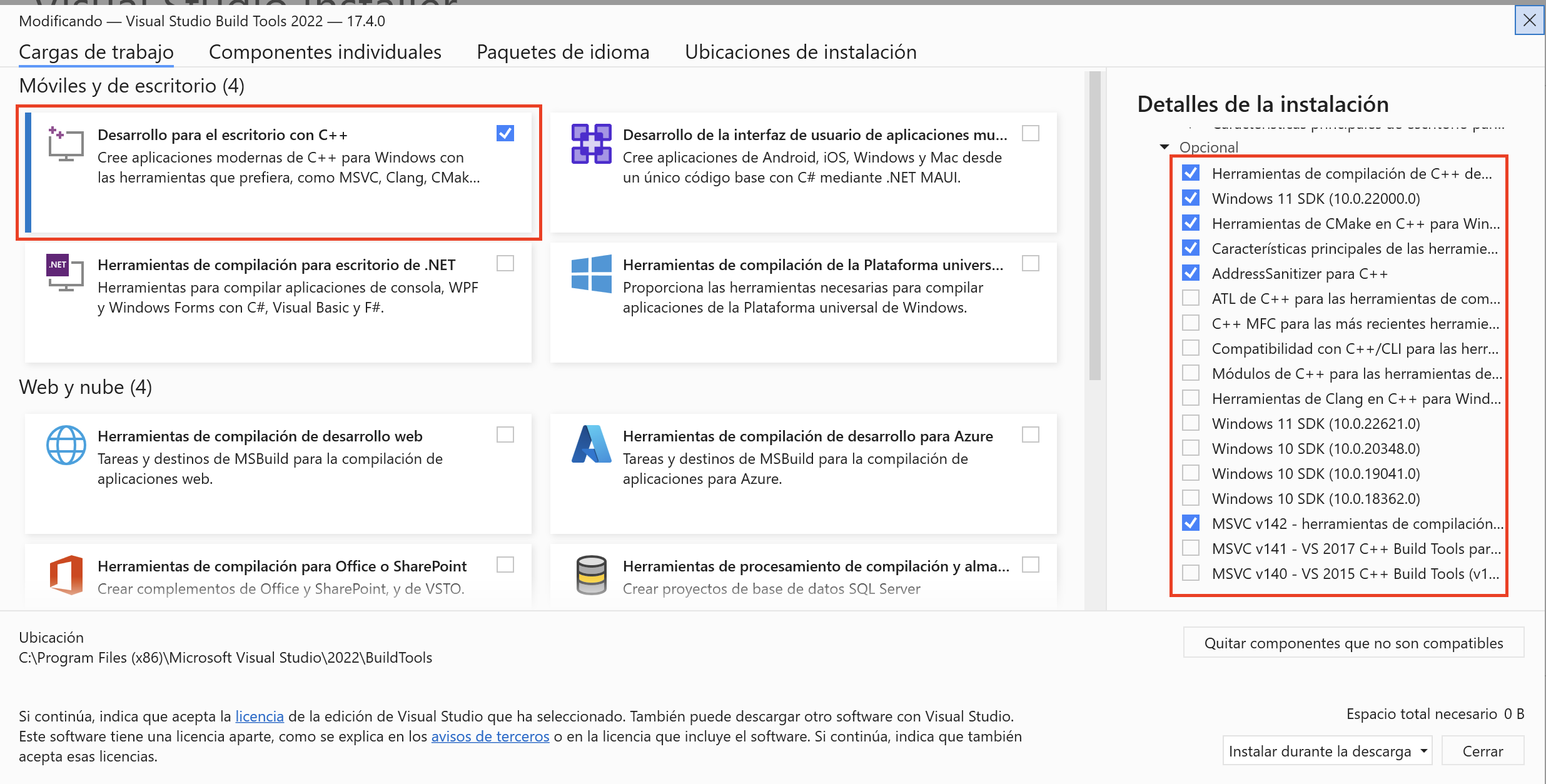

5. Install [Visual Studio Build Tools](https://visualstudio.microsoft.com/es/downloads/)

(Only for Windows).

[](https://riskfolio-lib.readthedocs.io/en/latest/_images/MVSC1.png)

[](https://riskfolio-lib.readthedocs.io/en/latest/_images/MVSC2.png)

6. Install `Riskfolio-lib`.

> `pip install riskfolio-lib`

7. To run some examples is necessary to install [yfinance](https://pypi.org/project/yfinance/)

.

> `pip install yfinance`

8. To run some examples is necessary to install MOSEK, you must follow [MOSEK](https://docs.mosek.com/9.2/install/installation.html)

installation instructions. To get a MOSEK license you must go to [Academic Licenses](https://www.mosek.com/products/academic-licenses/)

.

> `pip install mosek`

Dependencies[¶](https://riskfolio-lib.readthedocs.io/en/latest/install.html#dependencies "Link to this heading")

-----------------------------------------------------------------------------------------------------------------

Riskfolio-Lib has the following dependencies:

* numpy>=1.24.0

* pandas>=2.0.0

* matplotlib>=3.8.0

* clarabel>=0.6.0

* cvxpy>=1.5.2

* scikit-learn>=1.3.0

* statsmodels>=0.13.5

* arch>=7.0

* xlsxwriter>=3.1.2

* networkx>=3.0

* astropy>=5.1 (if there are problems check [astropy installation instructions](https://www.astropy.org/)

)

* pybind11>=2.10.1

---

# Examples - Riskfolio-Lib 7.2

[Skip to content](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#return-risk-portfolio-optimization-models)

Examples[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#examples "Link to this heading")

==========================================================================================================

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

The following examples are available:

Return Risk Portfolio Optimization Models[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#return-risk-portfolio-optimization-models "Link to this heading")

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

* [Mean Risk Portfolio Optimization using Historical Estimates](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%201%20-%20Classic%20Mean%20Risk%20Optimization.ipynb)

.

* [Mean Risk Portfolio Optimization using Custom Estimates (mean and covariance)](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%206%20-%20Portfolio%20Optimization%20with%20Custom%20Parameters.ipynb)

.

* [Ulcer Index Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2014%20-%20Mean%20Ulcer%20Index%20Portfolio%20Optimization.ipynb)

.

* [Entropic Value at Risk (EVaR) Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2015%20-%20Mean%20Entropic%20Value%20at%20Risk%20(EVaR)%20Optimization.ipynb)

.

* [Riskfolio-Lib with MOSEK for Real Applications (612 assets and 4943 observations)](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2017%20-%20Riskfolio-Lib%20with%20MOSEK%20for%20Real%20Applications%20(612%20assets%20and%204943%20observations).ipynb)

.

* [Entropic Drawdown at Risk (EDaR) Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2019%20-%20Mean%20Entropic%20Drawdown%20at%20Risk%20(EDaR)%20Optimization.ipynb)

.

* [Logarithmic Mean Risk (Kelly Criterion) Portfolio Optimization](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2022%20-%20Logarithmic%20Mean%20Risk%20Optimization%20(Kelly%20Criterion).ipynb)

.

* [Worst Case Mean Variance Portfolio Optimization using Box and Elliptical Uncertainty Sets](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2012%20-%20Worst%20Case%20Mean%20Variance%20Portfolio%20Optimization.ipynb)

.

* [Comparing Covariance Estimates Methods](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2034%20-%20Comparing%20Covariance%20Estimators%20Methods.ipynb)

.

* [Gini Mean Difference (GMD) Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2035%20-%20Gini%20Mean%20Difference%20(GMD)%20Optimization.ipynb)

.

* [Tail Gini Range Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2036%20-%20Mean%20Tail%20Gini%20Range%20Optimization.ipynb)

.

* [Ordered Weighted Averaging (OWA) Portfolio Optimization](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2037%20-%20OWA%20Portfolio%20Optimization.ipynb)

.

* [Kurtosis Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2038%20-%20Mean%20Kurtosis%20Optimization.ipynb)

.

* [Semi Kurtosis Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2039%20-%20Mean%20Semi%20Kurtosis%20Optimization.ipynb)

.

* [Relativistic Value at Risk (RLVaR) Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2040%20-%20Mean%20Relativistic%20Value%20at%20Risk%20(RLVaR)%20Optimization.ipynb)

.

* [Relativistic Drawdown at Risk (RLDaR) Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2041%20-%20Mean%20Relativistic%20Drawdown%20at%20Risk%20(RLDaR)%20Optimization.ipynb)

.

* [Higher L-Moments OWA Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2042%20-%20Higher%20L-Moments%20OWA%20Portfolio%20Optimization.ipynb)

.

* [Entropic Value at Risk Range (EVRG) Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2049%20-%20Mean%20Entropic%20Value%20at%20Risk%20Range%20(EVRG)%20Optimization.ipynb)

.

* [Relativistic Value at Risk Range (RVRG) Portfolio Optimization for Mean Risk and Risk Parity](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2050%20-%20Mean%20Relativistic%20Value%20at%20Risk%20Range%20(RVRG)%20Optimization.ipynb)

.

Special Constraints[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#special-constraints "Link to this heading")

--------------------------------------------------------------------------------------------------------------------------------

* [Index Tracking/Replicating Portfolios](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%207%20-%20Index%20Tracking-Replicating%20Portfolios.ipynb)

.

* [Short and Leveraged Portfolios](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%208%20-%20Short%20and%20Leveraged%20Portfolios.ipynb)

.

* [Portfolio Optimization with Constraints on Return and Risk Measures](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2021%20-%20Constraints%20on%20Return%20and%20Risk%20Measures.ipynb)

.

* [Portfolio Optimization with Dollar Neutral Constraint](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2023%20-%20Dollar%20Neutral%20Portfolios.ipynb)

.

* [Portfolio Optimization with Constraints on Number of Assets and Number of Effective Assets](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2026%20-%20Constraints%20on%20Maximum%20Number%20of%20Assets.ipynb)

.

* [Portfolio Optimization with Integer Constraints](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2052%20-%20Portfolio%20Optimization%20with%20Integer%20Constraints.ipynb)

.

Risk Factors Models[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#risk-factors-models "Link to this heading")

--------------------------------------------------------------------------------------------------------------------------------

* [Mean Risk Portfolio Optimization using Risk Factors and Stepwise Regression](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%202%20-%20Portfolio%20Optimization%20using%20Risk%20Factors%20and%20Stepwise%20Regression.ipynb)

.

* [Mean Risk Portfolio Optimization using Risk Factors and Principal Component Regression](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%209%20-%20Portfolio%20Optimization%20using%20Risk%20Factors%20and%20Principal%20Components%20Regression%20(PCR).ipynb)

.

* [Fixed Income Portfolio Optimization and Immunization](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%204%20-%20Bond%20Portfolio%20Optimization%20and%20Immunization.ipynb)

.

* [Vanilla Risk Parity Optimization using Risk Factors and Stepwise Regression](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2011%20-%20Risk%20Parity%20Portfolio%20Optimization%20using%20Risk%20Factors%20and%20Stepwise%20Regression.ipynb)

.

* [Mean Kurtosis Portfolio Optimization using Risk Factors](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2053%20-%20Mean%20Kurtosis%20Optimization%20using%20Risk%20Factors.ipynb)

.

Black Litterman Models[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#black-litterman-models "Link to this heading")

--------------------------------------------------------------------------------------------------------------------------------------

* [Mean Risk Portfolio Optimization using Black Litterman Model](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%203%20-%20Mean%20Risk%20Optimization%20using%20Black%20Litterman.ipynb)

.

* [Mean Risk Portfolio Optimization using Black Litterman Model and Risk Factors Models (Black Litterman Bayesian and Augmented Black Litterman)](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2020%20-%20Mean%20Risk%20Optimization%20using%20Black%20Litterman%20and%20Risk%20Factors%20Models.ipynb)

.

Risk Parity Models[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#risk-parity-models "Link to this heading")

------------------------------------------------------------------------------------------------------------------------------

* [Vanilla Risk Parity Portfolio Optimization using historical estimates](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2010%20-%20Risk%20Parity%20Portfolio%20Optimization.ipynb)

.

* [Relaxed Risk Parity Portfolio Optimization](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2032%20-%20Relaxed%20Risk%20Parity%20Portfolio%20Optimization.ipynb)

.

* [Risk Parity with Constraints using the Risk Budgeting Approach](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2033%20-%20Risk%20Parity%20with%20Constraints%20using%20the%20Risk%20Budgeting%20Approach.ipynb)

.

* [Risk Parity with a Risk Constraint per Classes](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2043%20-%20Risk%20Parity%20with%20a%20Risk%20Constraint%20per%20Classes.ipynb)

.

* [Risk Parity with Risk Factors](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2047%20-%20Risk%20Parity%20with%20Risk%20Factors.ipynb)

.

* [Mean Variance Portfolio Optimization with Risk Contribution Inequalities Constraints](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2048%20-%20Classic%20Mean%20Variance%20Optimization%20with%20Risk%20Contribution%20Inequalities%20Constraints.ipynb)

.

* [Mean Variance Portfolio Optimization with Risk Factor Contribution Inequalities Constraints](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2051%20-%20Classic%20Mean%20Variance%20Optimization%20with%20Risk%20Factor%20Contribution%20Inequalities%20Constraints.ipynb)

.

Hierarchical Clustering Portfolio Optimization[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#hierarchical-clustering-portfolio-optimization "Link to this heading")

--------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

* [Hierarchical Risk Parity (HRP) Portfolio Optimization](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2024%20-%20Hierarchical%20Risk%20Parity%20(HRP)%20Portfolio%20Optimization.ipynb)

.

* [Hierarchical Equal Risk Contribution (HERC) Portfolio Optimization](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2025%20-%20Hierarchical%20Equal%20Risk%20Contribution%20(HERC)%20Portfolio%20Optimization.ipynb)

.

* [Hierarchical Equal Risk Contribution with Equally Weights within Clusters (HERC2) Portfolio Optimization](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2027%20-%20HERC%20with%20Equal%20Weights%20within%20Clusters%20(HERC2).ipynb)

.

* [Hierarchical Risk Parity with Constraints](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2029%20-%20Hierarchical%20Risk%20Parity%20(HRP)%20Portfolio%20Optimization%20with%20Constraints.ipynb)

.

* [Nested Clustered Optimization (NCO)](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2030%20-%20Nested%20Clustered%20Optimization%20(NCO).ipynb)

.

* [Hierarchical Portfolios with Custom Covariance](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2031%20-%20Hierarchical%20Portfolios%20with%20Custom%20Covariance.ipynb)

.

* [Hierarchical Equal Risk Contribution (HERC) with Constraints](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2044%20-%20Hierarchical%20Equal%20Risk%20Contribution%20(HERC)%20Portfolio%20Optimization%20with%20Constraints.ipynb)

.

* [Nested Clustered Optimization (NCO) with Constraints](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2045%20-%20Nested%20Clustered%20Optimization%20(NCO)%20Portfolio%20Optimization%20with%20Constraints.ipynb)

.

Graph Theory Constraints[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#graph-theory-constraints "Link to this heading")

------------------------------------------------------------------------------------------------------------------------------------------

* [Hierarchical Clustering and Networks](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2028%20-%20Hierarchical%20Clustering%20and%20Networks.ipynb)

.

* [Classic Mean Risk Optimization with Network and Dendrogram Constraints](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2046%20-%20Classic%20Mean%20Risk%20Optimization%20with%20Network%20and%20Dendrogram%20Constraints.ipynb)

.

Backtesting[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#backtesting "Link to this heading")

----------------------------------------------------------------------------------------------------------------

* [Multi Assets Algorithmic Trading Backtesting using Backtrader](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%205%20-%20Multi%20Assets%20Algorithmic%20Trading%20Backtesting%20with%20Backtrader.ipynb)

(matplotlib=3.2.2 for compatibility with backtrader=1.9.76.123. We don’t recommend to try to reproduce this example due the compatibility problems of Backtrader).

* [Multi Assets Algorithmic Trading Backtesting using Vectorbt](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2018%20-%20Multi%20Assets%20Algorithmic%20Trading%20Backtesting%20with%20Vectorbt.ipynb)

(vectorbt=0.26.1).

Excel and Reporting[¶](https://riskfolio-lib.readthedocs.io/en/latest/examples.html#excel-and-reporting "Link to this heading")

--------------------------------------------------------------------------------------------------------------------------------

* [Riskfolio-Lib and Xlwings](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2013%20-%20Riskfolio-Lib%20and%20Xlwings.ipynb)

.

* [Riskfolio-Lib Reports in Jupyter Notebook and Excel](https://colab.research.google.com/github/dcajasn/Riskfolio-Lib/blob/master/examples/Tutorial%2016%20-%20Riskfolio-Lib%20Reports%20in%20Jupyter%20Notebook%20and%20Excel.ipynb)

.

---

# Authors - Riskfolio-Lib 7.2

Authors[¶](https://riskfolio-lib.readthedocs.io/en/latest/authors.html#authors "Link to this heading")

=======================================================================================================

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

* **Dany Cajas**

I’m a BSc in Economic Engineering at Universidad Nacional de Ingeniería and MA in Finance at Universidad del Pacífico. I am very interested in quantitative finance. For more about me, you can visit:

* My blog [financioneroncios](https://financioneroncios.wordpress.com/)

.

* My [linkedin](https://www.linkedin.com/in/dany-cajas/)

.

* My [SSRN author page](https://papers.ssrn.com/sol3/cf_dev/AbsByAuth.cfm?per_id=2931756)

where you can find all my working papers.

* Or write me to [dcajasn@gmail.com](mailto:dcajasn%40gmail.com)

.

I like to learn and apply my knowledge in practical applications; for this reason, I started my blog to practice and share in my native language the things that I’ve been learned until now. One topic that always have been very interesting to me is portfolio optimization. However, I realized that open-source libraries (python) are few (there are among one and four) and are mainly focused on mean variance optimization, ignoring advances in other convex risk measures (CVaR, MAD, Maximum Drawdown, etc.) and other estimations techniques like robust estimates, Black Litterman and risk factors models. For this reason, I developed Riskfolio-Lib, a well documented library that will help students, academics and practitioners to apply mathematically complex optimization models in their strategic asset allocation process.

---

# Contributing - Riskfolio-Lib 7.2

[Skip to content](https://riskfolio-lib.readthedocs.io/en/latest/contributing.html#how-to-contribute)

Contributing[¶](https://riskfolio-lib.readthedocs.io/en/latest/contributing.html#contributing "Link to this heading")

======================================================================================================================

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

How to contribute?[¶](https://riskfolio-lib.readthedocs.io/en/latest/contributing.html#how-to-contribute "Link to this heading")

---------------------------------------------------------------------------------------------------------------------------------

I would like to people help me to:

* Improve documentation.

* Improve performance of existing code.

* Add new optimization objectives functions, robust estimation techniques or new functionalities.

* Write more examples using jupyter notebooks.

* Help me to write tests using pytest.

* Recommend new journal papers, articles, blog posts related to convex portfolio optimization that you think will improve the features of Riskfoli-Lib.

Do you have any questions?[¶](https://riskfolio-lib.readthedocs.io/en/latest/contributing.html#do-you-have-any-questions "Link to this heading")

-------------------------------------------------------------------------------------------------------------------------------------------------

If you have any questions related to Riskfolio-Lib, please [raise an issue](https://github.com/dcajasn/Riskfolio-Lib/issues)

and I will tag it as a question.

If you have questions _unrelated_ to Riskfolio-Lib or want advisory, contact me through my blog [financioneroncios](https://financioneroncios.wordpress.com/)

, my [linkedin](https://www.linkedin.com/in/dany-cajas/)

or write me an email to [dany.cajas.n@uni.pe](mailto:dany.cajas.n%40uni.pe)

---

# License - Riskfolio-Lib 7.2

License[¶](https://riskfolio-lib.readthedocs.io/en/latest/license.html#license "Link to this heading")

=======================================================================================================

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

Copyright (c) 2020-2026, Dany Cajas All rights reserved.

Redistribution and use in source and binary forms, with or without modification, are permitted provided that the following conditions are met:

* Redistributions of source code must retain the above copyright notice, this list of conditions and the following disclaimer.

* Redistributions in binary form must reproduce the above copyright notice, this list of conditions and the following disclaimer in the documentation and/or other materials provided with the distribution.

* Neither the name of Riskfolio-Lib nor the names of its contributors may be used to endorse or promote products derived from this software without specific prior written permission.

THIS SOFTWARE IS PROVIDED BY THE COPYRIGHT HOLDERS AND CONTRIBUTORS “AS IS” AND ANY EXPRESS OR IMPLIED WARRANTIES, INCLUDING, BUT NOT LIMITED TO, THE IMPLIED WARRANTIES OF MERCHANTABILITY AND FITNESS FOR A PARTICULAR PURPOSE ARE DISCLAIMED. IN NO EVENT SHALL THE COPYRIGHT HOLDER OR CONTRIBUTORS BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, SPECIAL, EXEMPLARY, OR CONSEQUENTIAL DAMAGES (INCLUDING, BUT NOT LIMITED TO, PROCUREMENT OF SUBSTITUTE GOODS OR SERVICES; LOSS OF USE, DATA, OR PROFITS; OR BUSINESS INTERRUPTION) HOWEVER CAUSED AND ON ANY THEORY OF LIABILITY, WHETHER IN CONTRACT, STRICT LIABILITY, OR TORT (INCLUDING NEGLIGENCE OR OTHERWISE) ARISING IN ANY WAY OUT OF THE USE OF THIS SOFTWARE, EVEN IF ADVISED OF THE POSSIBILITY OF SUCH DAMAGE.

---

# Changelog - Riskfolio-Lib 7.2

[Skip to content](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-7-2-0)

Changelog[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#changelog "Link to this heading")

=============================================================================================================

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

Version 7.2.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-7-2-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Add functions that allow to calculate estimators of coskewness tensor and cokurtosis square matrix based on risk factor models.

* Add the possibility to optimize portfolio kurtosis using an estimator of cokurtosis square matrix based on risk factor models.

* Add the possibility to add constraints on portfolio kurtosis using an estimator of cokurtosis square matrix based on risk factor models.

Version 7.1.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-7-1-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Add the possibility to included integer constraints such as cardinality constraints on assets and categories, mutually exclusive constraints and join investment constraints in the portfolio object.

* Add a new helper function that allows users to create the matrices that represent the integer constraints.

* Fixed a bug related to leverage portfolios.

Version 7.0.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-7-0-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Add two new convex risk measures: EVaR Range and RLVaR Range, to the Portfolio object.

* Add three new risk measures: VaR Range, EVaR Range and RLVaR Range, to the HCPortfolio object.

* Add the generalization of risk parity for variance through inequality constraints on the risk contributions of assets to the Portfolio object.

* Add the generalization of factor risk parity for variance through inequality constraints on the risk contributions of risk factors to the Portfolio object.

* Add a function to calculate the Brinson Performance Attribution per class and aggregate.

* Add a plot function to show the Brinson Performance Attribution.

* Add functions to calculate the VaR Range, EVaR Range and RLVaR Range.

* Update plot functions to consider EVaR Range and RLVaR Range.

* Update duplication, elimination and summation matrices functions to consider or not the diagonal of the symmetric matrix.

Version 6.3.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-6-3-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Add new functions to calculate the number of effective assets (NEA) and the average centrality of the portfolio.

* Add the possibility to use neighborhood and cluster network constraints at the same time.

* Fixed some bugs in HRP and HERC when we add constraints.

* Fixed a bug in the duplication\_summation\_matrix.

* Fixed tight layout in plot functions that uses multiple axes.

Version 6.2.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-6-2-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Improvement in calculation speed of duplication\_matrix, duplication\_elimination\_matrix and duplication\_summation\_matrix functions using a vectorized formula.

* Fixed formulation of risk parity with risk factors model that produced incorrect results when using the MOSEK solver.

* Fixed some bugs in PlotFunctions module.

* Fixed some bugs in HCPortfolio related to custom\_mu vector and use of Kurtosis and Semi Kurtosis as risk measures.

* Standardized the way additional parameters to estimate mean vector and covariance matrix are entered.

Version 6.1.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-6-1-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements standarized silhouette score to determine the optimal number of clusters.

* Fix plot\_clusters function to plot clusters and heatmap in same order of codependence matrix. Originally it plots the codependece matrix with axis x inverted.

Version 6.0.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-6-0-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements risk parity optimization based on explicit risk factors and principal components.

* Implements new formulations of Gini Mean Difference, Tail Gini, Range, CVaR Range and Tail Gini Range that improves speed compared to formulations based on the owa portfolio model.

* Improves the calculation of elliptical uncertainty sets for worst case optimization.

* Add new functions that allow us to calculate the risk contribution per explicit risk factors and principal components.

* Add new functions that allow us to plot the risk contribution per explicit risk factors and principal components.

Version 5.0.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-5-0-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements new kind of constraints that incorporates the information from networks like the Minimum Spanning Tree and Maximally Filtered Graph into the portfolio optimization models: return-risk portfolio, owa portfolio and worst case portfolio.

* Implements new kind of constraints that incorporates the information from dendrograms into the portfolio optimization models: return-risk portfolio, owa portfolio and worst case portfolio.

* Improves the speed of several functions using the c++ linear algebra library Eigen and c++ eigenvalues library Spectra.

* Add new functions that allow us to plot the relationship between graphs and asset allocation.

* Add new functions that allow us to create constraints based on graphs information.

* Add a new example about applications of networks and dendrograms constraints in portfolio optimization problems.

* Fixed some errors related to HCPortfolio with constraints.

* Fixed some errors in some plots.

Version 4.4.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-4-4-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements the approximate Kurtosis model through sum of squared quadratic forms for large scale kurtosis optimization.

* Add the block vectorization operator.

Version 4.3.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-4-3-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements custom constraints for the Relaxed Risk Parity portfolio model.

* Add three new methods to estimate the mean vector: James-Stein, Bayes-Stein and BOP.

Version 4.2.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-4-2-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements constraints for the Hierarchical Equal Risk Contribution (HERC) and Nested Clustered Optimization (NCO) portfolio models.

* Add the option to show risk contributions as a percentage of total risk in risk contribution plot.

* Repairs some bugs.

Version 4.1.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-4-1-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements the Relativistic Value at Risk and Relativistic Drawdown at Risk portfolio models.

* Implements the Higher L-moments portfolio model function as an special case of OWA portfolio.

* Adds functions to calculate L-moments.

* Adds a function to calculate risk contribution constraints on asset classes.

* Repairs some bugs.

Version 4.0.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-4-0-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements Kurtosis and Semi Kurtosis portfolio models based on parametric approach.

* Implements new c++ based functions to speed up kurtosis model calculations.

* Repairs some bugs.

Version 3.3.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-3-3-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Adds Kendall Tau and Gerber statistic as options for codependence matrix in HCPortfolio object.

* Adds Gerber statistic as an option for covariance matrix estimator in Portfolio and HCPortfolio objects.

Version 3.2.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-3-2-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements reformulations of portfolio models based on drawdowns to speed up calculations.

* Adds some tests for portfolio object and hcportfolio object.

Version 3.1.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-3-1-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements a reformulation of OWA portfolio optimization to speed up calculations.

Version 3.0.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-3-0-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements 5 additional risk measures for mean risk model: Gini Mean Difference, Tail Gini, Range, CVaR range and Tail Gini range.

* Implements 4 additional risk measures for risk parity model: Gini Mean Difference, Tail Gini, CVaR range and Tail Gini range.

* Implements the OWA Portfolio Optimization model for custom vector of weights and a module to build OWA weights for some special cases.

* Implements a function to plot range risk measures.

* Adds the option to use Graphical Lasso, j-Logo, denoising and detoning covariance estimates.

Version 2.0.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-2-0-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implement Nested Clustered Optimization (NCO) model with four objective functions.

* Implements the Relaxed Risk Parity model.

* Implements the Risk Budgeting approach for Risk Parity Portfolios with constraints.

* Adds the option to use custom covariance in Hierarchical Clustering Portfolios.

Version 1.0.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-1-0-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Redesigns of Riskfolio-Lib interface (Only import riskfolio for all functions).

* Implements Hierarchical Risk Parity (HRP) model with constraints on assets’ weights.

* Implements a function that helps to build constraints for the HRP model.

* Implements the Direct Bubble Hierarchical Tree (DBHT) linkage method for HRP and HERC models.

* Implements a function that plots relationship among assets in a network using Minimum Spanning Tree (MST) and Planar Maximally Filtered Graph (PMFG).

* Adds two new codependence measures: mutual information and lower tail dependence index.

Version 0.4.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-4-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements Hierarchical Equal Risk Contribution with equally weights within clusters (HERC2).

* Implements a function that help us to discretize portfolio weights into number of shares given an investment amount.

* Implements the option to select the method to estimate covariance in HRP, HERC and HERC2.

* Adds the option to add constraints on the number of assets and the number of effective assets.

* Fixes an error in two\_diff\_gap\_stat() when number of assets is too small.

* Fixes an error on forward\_regression() and backward\_regression() when there is no significant feature in regression modes using p-value criterion.

* Adds an example that shows how to build HERC2 portfolios.

* Adds an example that shows how to build constraints on the number of assets and number of effective assets.

Version 0.3.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-3-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements Hierarchical Risk Parity (HRP) and Hierarchical Equal Risk Parity (HERC).

* Implements the function plot\_clusters() and plot\_dendrogram() that help us to identify clusters based on a distance correlation metric.

* Implements the function assets\_clusters() that help us to create asset classes based on hierarchical clusters.

* Adds an example that shows how to build Hierarchical Risk Parity portfolios.

* Adds an example that shows how to build Hierarchical Equal Risk Parity portfolios.

Version 0.2.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-2-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements Logarithmic Mean Risk (Kelly Criterion) Portfolio Optimization models.

* Implements the function plot\_bar() that help us to plot portfolios with negative weights.

* Adds the option to build dollar neutral portfolios.

* Adds an example that shows how to build Logarithmic Mean Risk (Kelly Criterion) portfolios.

* Adds an example that shows how to build dollar neutral portfolios.

Version 0.1.5[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-1-5 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Adds the option to add a constraint on minimum portfolio return.

* Adds an example of how to add constraints on portfolio return and risk measures.

Version 0.1.4[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-1-4 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Adds Black Litterman with factors in two flavors: Black Litterman Bayesian model and Augmented Black Litterman model.

* Implements factors\_views, a function that allows to design views on risk factors for Black Litterman with factors.

* Repairs some bugs.

Version 0.1.2[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-1-2 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Adds Entropic Drawdown at Risk for Mean Risk Portfolio Optimization and Risk Parity Portfolio Optimization.

* Repairs some bugs.

Version 0.1.1[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-1-1 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Repairs some bugs in Portfolio related to Semi Variance and UCI.

* Implements an option to annualize returns and risk in plot\_frontier, Jupyter Notebook and Excel reports.

* Adds examples using Vectorbt for Backtesting and MOSEK for large scale problems.

Version 0.1.0[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-1-0 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Repairs some bugs in RiskFunctions.

* Implements the Reports module that helps to build reports on Jupyter Notebook and Excel.

* Implements plot\_table, a function that resume some indicators of a portfolio.

* Adds Entropic Value at Risk for Mean Risk Portfolio Optimization and Risk Parity Portfolio Optimization.

Version 0.0.7[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-0-7 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements normal assumption method to estimate box and elliptical uncertainty sets for Worst Case Optimization.

* Implements elliptical uncertainty sets for covariance matrix.

* Adds Ulcer Index for Mean Risk Portfolio Optimization and Risk Parity Portfolio Optimization.

* Implements functions to calculate Ulcer Index.

Version 0.0.6[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-0-6 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Repairs some bugs.

* Implements bootstrapping methods to estimate box and elliptical uncertainty sets for Worst Case Optimization.

* Implements Worst Case Mean Variance Portfolio Optimization using box and elliptical uncertainty sets.

Version 0.0.5[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-0-5 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Repairs some bugs.

* Implements Risk Parity Portfolio Optimization for 7 convex risk measures.

Version 0.0.4[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-0-4 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Repairs some bugs.

* Update to make it compatible with cvxpy >=1.1.0

* Implements Principal Component Regression for loadings matrix estimation.

* Adds Akaike information criterion, Schwarz information criterion, R squared and adjusted R squared feature selection criterions in stepwise regression.

Version 0.0.3[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-0-3 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Repairs some bugs.

* Implements an option for building constraints common for all assets classes.

Version 0.0.2[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-0-2 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Repairs some bugs.

Version 0.0.1[¶](https://riskfolio-lib.readthedocs.io/en/latest/changelog.html#version-0-0-1 "Link to this heading")

---------------------------------------------------------------------------------------------------------------------

* Implements robust and ewma estimates.

* Implements Black Litterman model and risk factors models.

* Implements mean risk optimization with 10 risk measures.

---

# Reports Functions - Riskfolio-Lib 7.2

[Skip to content](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#example)

Reports Functions[¶](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#reports-functions "Link to this heading")

===========================================================================================================================

[Buy Advanced Portfolio Optimization Book on Springer](https://www.kqzyfj.com/click-101359873-15150084?url=https%3A%2F%2Flink.springer.com%2Fbook%2F9783031843037)

[Enroll in the Portfolio Optimization with Python Course](https://www.paypal.com/ncp/payment/GN55W4UQ7VAMN)

[](https://github.com/sponsors/dcajasn)

[](https://ko-fi.com/B0B833SXD)

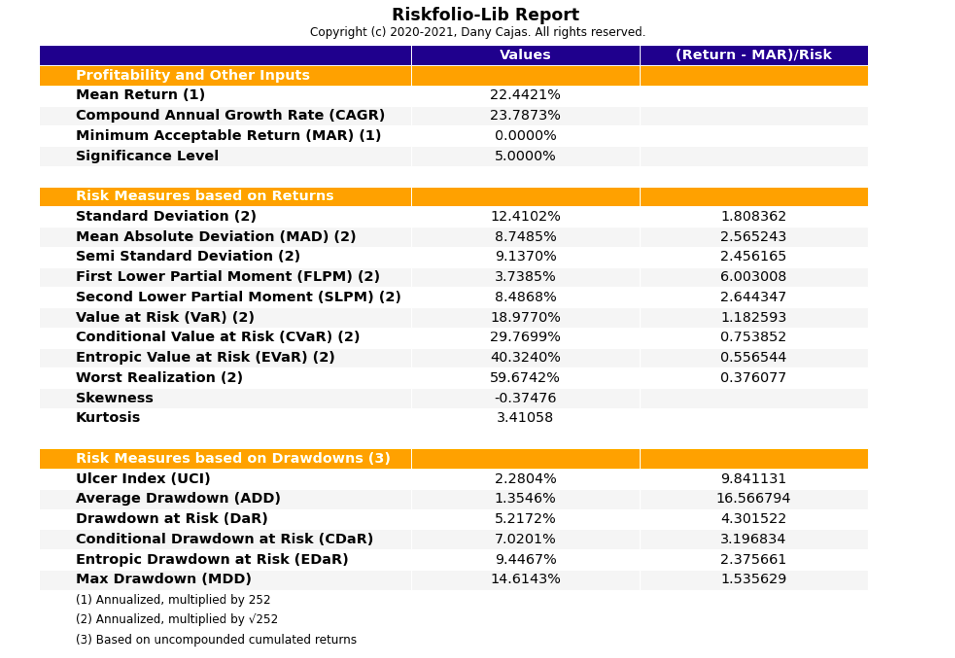

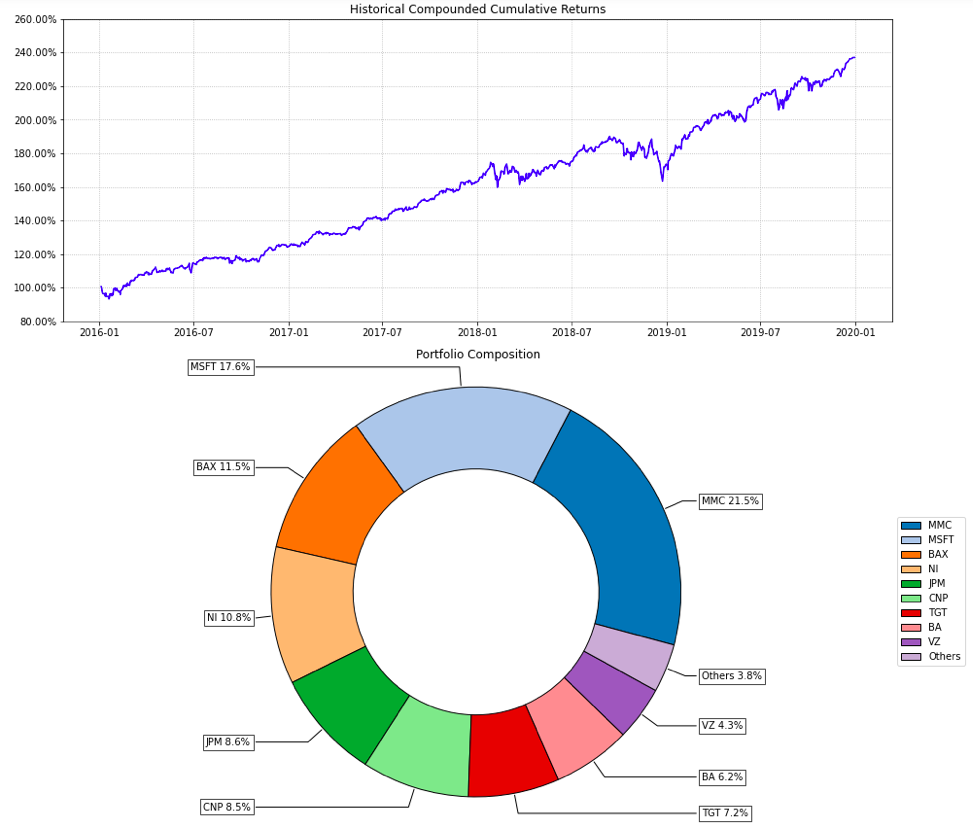

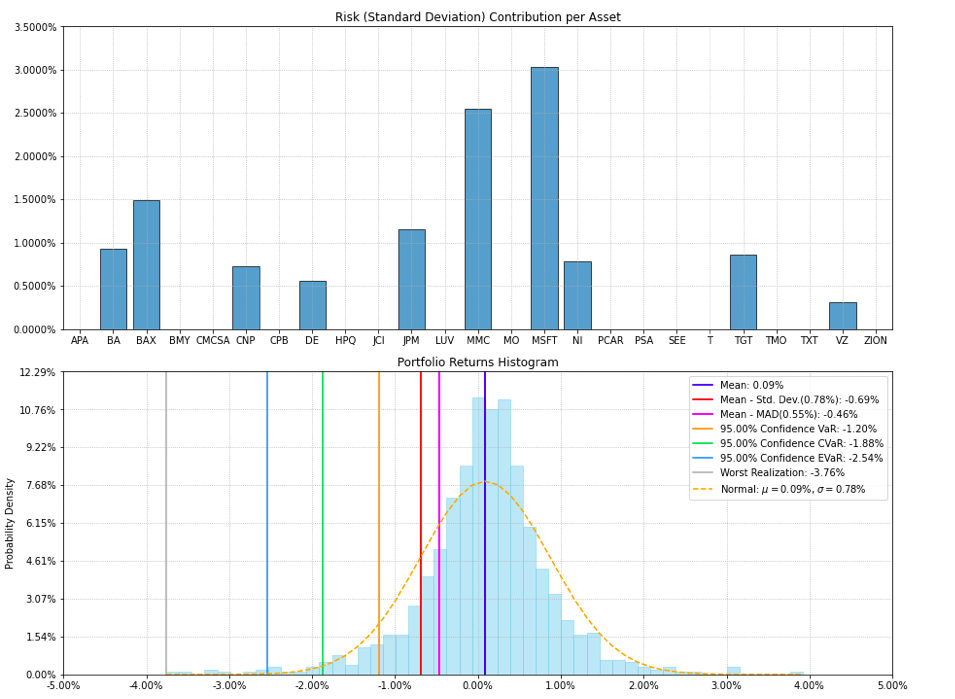

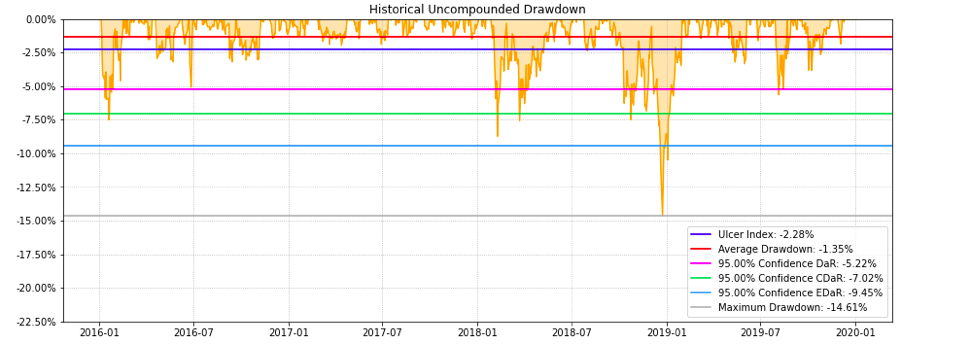

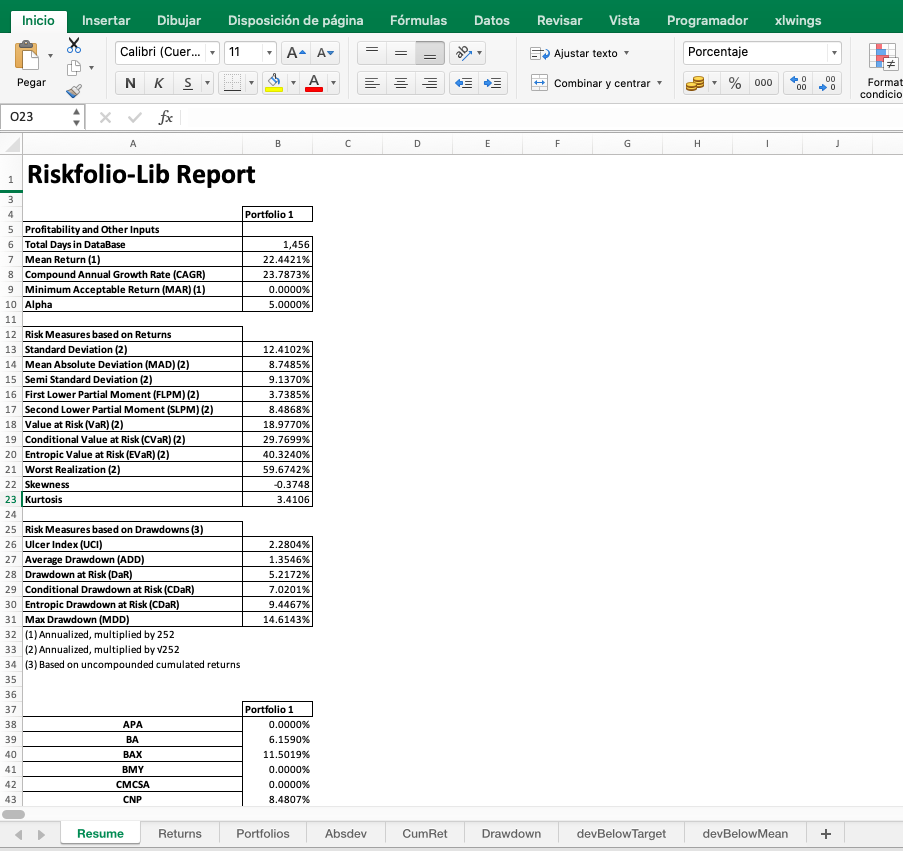

This section explains some functions that allows us to create Jupyter Notebook and Excel reports that helps us to analyze quickly the properties of our portfolios.

The following example build an optimum portfolio and create a Jupyter Notebook and Excel report using the functions of this module.

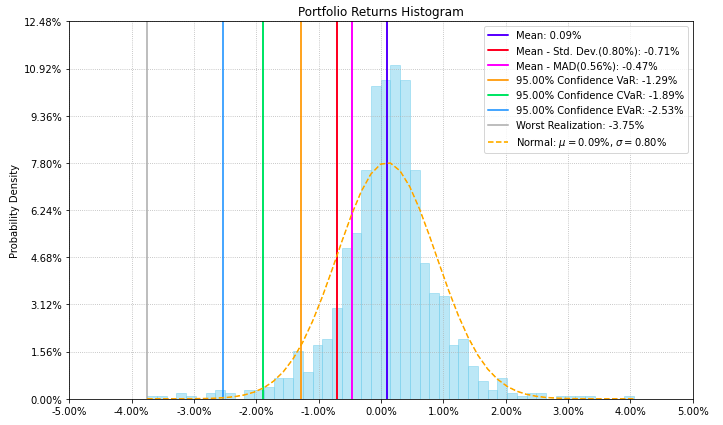

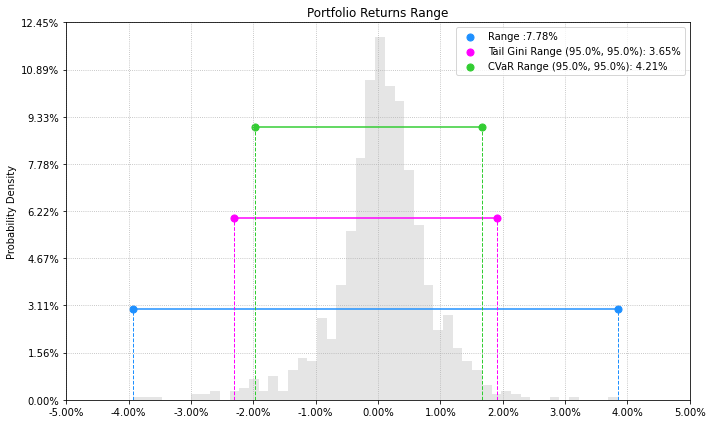

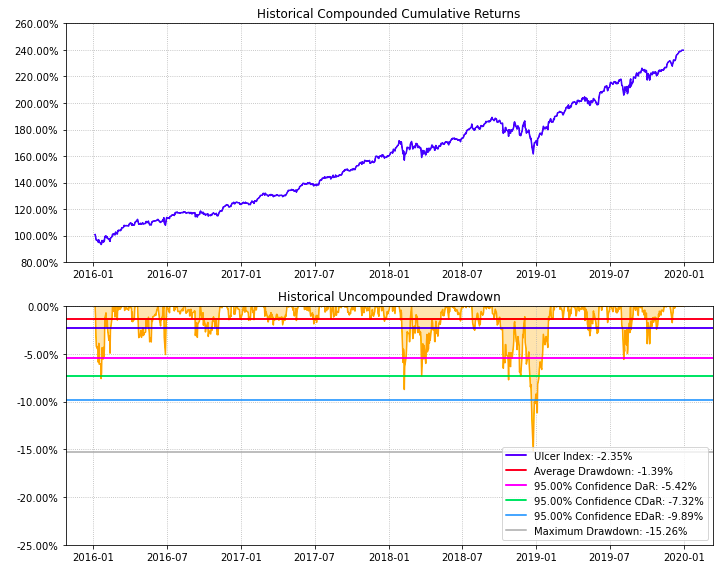

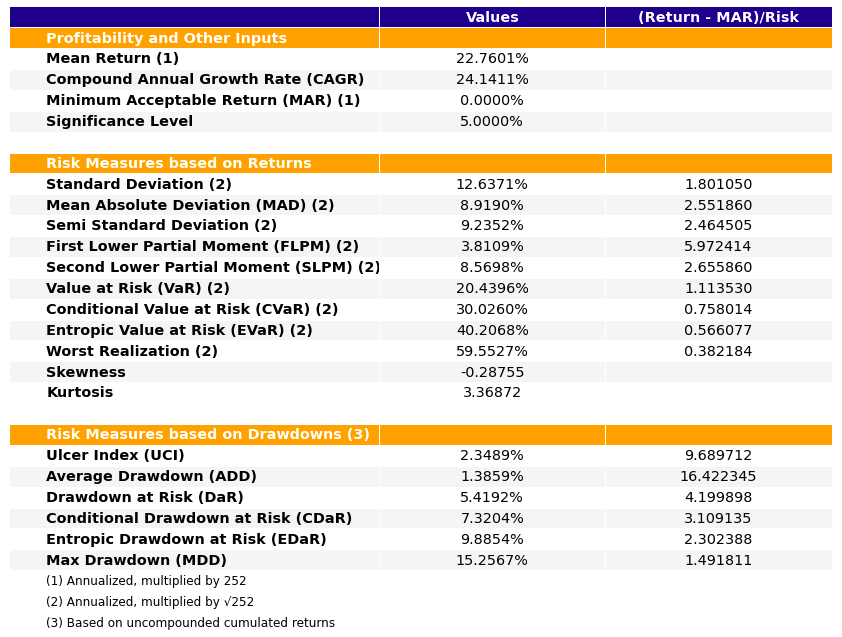

Example[¶](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#example "Link to this heading")

-------------------------------------------------------------------------------------------------------

`import numpy as np import pandas as pd import yfinance as yf import riskfolio as rp yf.pdr_override() # Date range start = '2016-01-01' end = '2019-12-30' # Tickers of assets tickers = ['JCI', 'TGT', 'CMCSA', 'CPB', 'MO', 'APA', 'MMC', 'JPM', 'ZION', 'PSA', 'BAX', 'BMY', 'LUV', 'PCAR', 'TXT', 'TMO', 'DE', 'MSFT', 'HPQ', 'SEE', 'VZ', 'CNP', 'NI', 'T', 'BA'] tickers.sort() # Downloading the data data = yf.download(tickers, start = start, end = end) data = data.loc[:,('Adj Close', slice(None))] data.columns = tickers assets = data.pct_change().dropna() Y = assets # Creating the Portfolio Object port = rp.Portfolio(returns=Y) # To display dataframes values in percentage format pd.options.display.float_format = '{:.4%}'.format # Choose the risk measure rm = 'MV' # Standard Deviation # Estimate inputs of the model (historical estimates) method_mu='hist' # Method to estimate expected returns based on historical data. method_cov='hist' # Method to estimate covariance matrix based on historical data. port.assets_stats(method_mu=method_mu, method_cov=method_cov) # Estimate the portfolio that maximizes the risk adjusted return ratio w = port.optimization(model='Classic', rm=rm, obj='Sharpe', rf=0.0, l=0, hist=True)`

Module Functions[¶](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#module-Reports "Link to this heading")

-----------------------------------------------------------------------------------------------------------------------

Reports.jupyter\_report(_[returns](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.returns "Reports.jupyter_report.returns (Python parameter) — Assets returns DataFrame, where n_samples is the number of observations and n_assets is the number of assets.")

_, _[w](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.w "Reports.jupyter_report.w (Python parameter) — Portfolio weights, where n_assets is the number of assets.")

_, _[rm](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.rm "Reports.jupyter_report.rm (Python parameter) — Risk measure used to estimate risk contribution. The default is 'MV'.")

\=`'MV'`_, _[rf](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.rf "Reports.jupyter_report.rf (Python parameter) — Risk free rate or minimum acceptable return.")

\=`0`_, _[alpha](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.alpha "Reports.jupyter_report.alpha (Python parameter) — Significance level of VaR, CVaR, Tail Gini, EVaR, RLVaR, CDaR, EDaR and RLDaR.")

\=`0.05`_, _[a\_sim](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.a_sim "Reports.jupyter_report.a_sim (Python parameter) — Number of CVaRs used to approximate Tail Gini of losses.")

\=`100`_, _[beta](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.beta "Reports.jupyter_report.beta (Python parameter) — Significance level of CVaR and Tail Gini of gains.")

\=`None`_, _[b\_sim](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.b_sim "Reports.jupyter_report.b_sim (Python parameter) — Number of CVaRs used to approximate Tail Gini of gains.")

\=`None`_, _[kappa](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.kappa "Reports.jupyter_report.kappa (Python parameter) — Deformation parameter of RLVaR and RLDaR, must be between 0 and 1.")

\=`0.3`_, _[solver](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.solver "Reports.jupyter_report.solver (Python parameter) — Solver available for CVXPY that supports power cone programming and exponential cone programming. Used to calculate EVaR, EDaR, RLVaR and RLDaR.")

\=`'CLARABEL'`_, _[percentage](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.percentage "Reports.jupyter_report.percentage (Python parameter) — If risk contribution per asset is expressed as percentage or as a value.")

\=`False`_, _[erc\_line](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.erc_line "Reports.jupyter_report.erc_line (Python parameter) — If equal risk contribution line is plotted. The default is False.")

\=`True`_, _[color](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.color "Reports.jupyter_report.color (Python parameter) — Color used to plot each asset risk contribution. The default is 'tab:blue'.")

\=`'tab:blue'`_, _[erc\_linecolor](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.erc_linecolor "Reports.jupyter_report.erc_linecolor (Python parameter) — Color used to plot equal risk contribution line. The default is 'r'.")

\=`'r'`_, _[others](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.others "Reports.jupyter_report.others (Python parameter) — Percentage of others section.")

\=`0.05`_, _[nrow](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.nrow "Reports.jupyter_report.nrow (Python parameter) — Number of rows of the legend.")

\=`25`_, _[cmap](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.cmap "Reports.jupyter_report.cmap (Python parameter) — Color scale used to plot each asset weight. The default is 'tab20'.")

\=`'tab20'`_, _[height](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.height "Reports.jupyter_report.height (Python parameter) — Average height of charts in the image in inches.")

\=`6`_, _[width](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.width "Reports.jupyter_report.width (Python parameter) — Width of the image in inches.")

\=`14`_, _[t\_factor](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.t_factor "Reports.jupyter_report.t_factor (Python parameter) — Factor used to annualize expected return and expected risks for risk measures based on returns (not drawdowns).")

\=`252`_, _[ini\_days](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.ini_days "Reports.jupyter_report.ini_days (Python parameter) — If provided, it is the number of days of compounding for first return. It is used to calculate Compound Annual Growth Rate (CAGR).")

\=`1`_, _[days\_per\_year](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.days_per_year "Reports.jupyter_report.days_per_year (Python parameter) — Days per year assumption.")

\=`252`_, _[bins](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report.bins "Reports.jupyter_report.bins (Python parameter) — Number of bins of the histogram.")

\=`50`_)[\[source\]](https://riskfolio-lib.readthedocs.io/en/latest/_modules/Reports.html#jupyter_report)

[¶](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report "Link to this definition")

Create a matplotlib report with useful information to analyze risk and profitability of investment portfolios.

Parameters:[¶](https://riskfolio-lib.readthedocs.io/en/latest/reports.html#Reports.jupyter_report-parameters "Permalink to this headline")